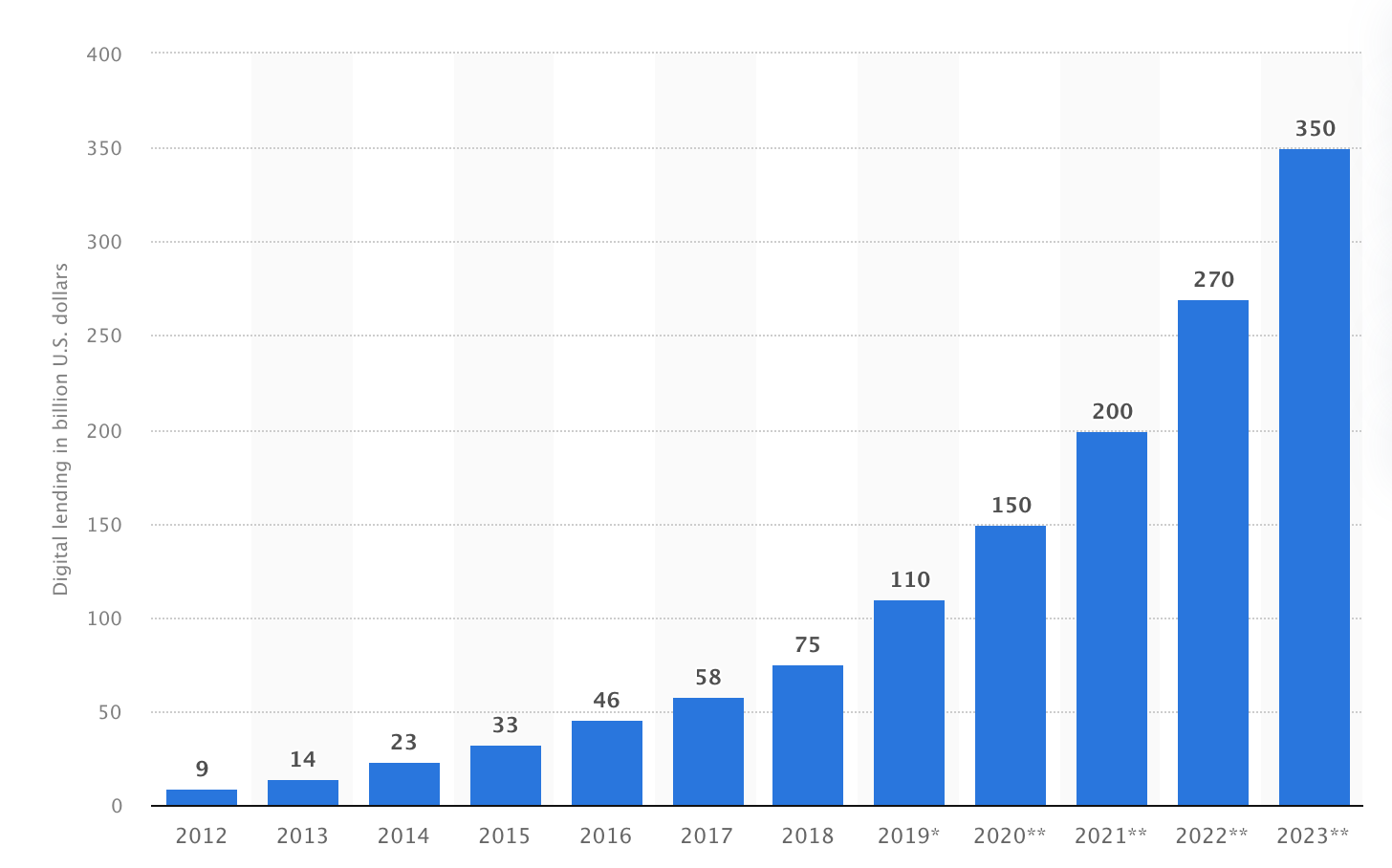

Digital lending is undoubtedly one of the fastest-growing industries globally, and over the years, observers have continuously noted India’s presence as the hub of this rapid growth. In 2019, the global research and analytics firm Statista benchmarked India’s digital lending industry at 110 Billion USD and in a follow-up infographic released in 2021, it was predicted that the industry would reach a cumulative valuation of 350 Billion USD by the end of 2023.

Along with this, over the past decade, several peer reviewed research papers and journals have continuously highlighted the rapid rise of India’s digital lending industry, and it begs the question about the factors which are the driving force behind this rise.

Thus, in today’s blog post, we will take a closer look at the 5 key factors which, in my opinion, have influenced the rapid growth of this industry and also try to understand the road that lies ahead.

Without further ado, let’s get started.

- Rise of Cheap Internet

Prior to the introduction of low-cost data carriers like Reliance Jio and Airtel, a significant portion of India’s populace was constrained by low internet speeds, both broadband and digital. However, since the introduction of low-cost data in 2016, internet usage has skyrocketed both among digital-savvy millennials as well as the older generation. Along with unhindered access to fast internet, smartphone prices have also significantly decreased, both of which combined has equipped the average consumer to explore the world of India’s internet, which among other industries, hosts the digital lending industry as well.

2. Increased Awareness

Since time immemorial, finances have been a taboo topic for discussion in India. Although a majority of Indians are now familiar with lending instruments, there was a time not too long ago when financial awareness among the general public was close to non-existence.

While a significant portion of this lack of awareness stems from the societal stigma of not discussing one’s finances, the advent of low-cost internet along with the rise of digital lenders have significantly contributed to the rise in consumer’s awareness about digital lending products and providers of the same.

For instance, 5 years back, the only form of loan my parents and me were aware of were those facilitated by SCBs such as SBI and Axis, however today, my parents are not only aware of personal loans and credit lines disbursed by digital lenders, but also rely on them from time to time for urgent or unforeseen expenditures.

3. Decreased Cost of Infrastructure

As I shared in an earlier point, along with easy access to cheap internet, another catalyst behind the meteoric rise of digital lending in India is the advent and streamlined availability of low-cost smartphones.

For instance, back in 2013, if you wanted to procure a smartphone, you needed to spend a minimum of ₹15,000 to get one; however, today, with so many low-cost hardware manufacturers in the market, you can get a top-notch smartphone with advanced capabilities at a fraction of the cost.

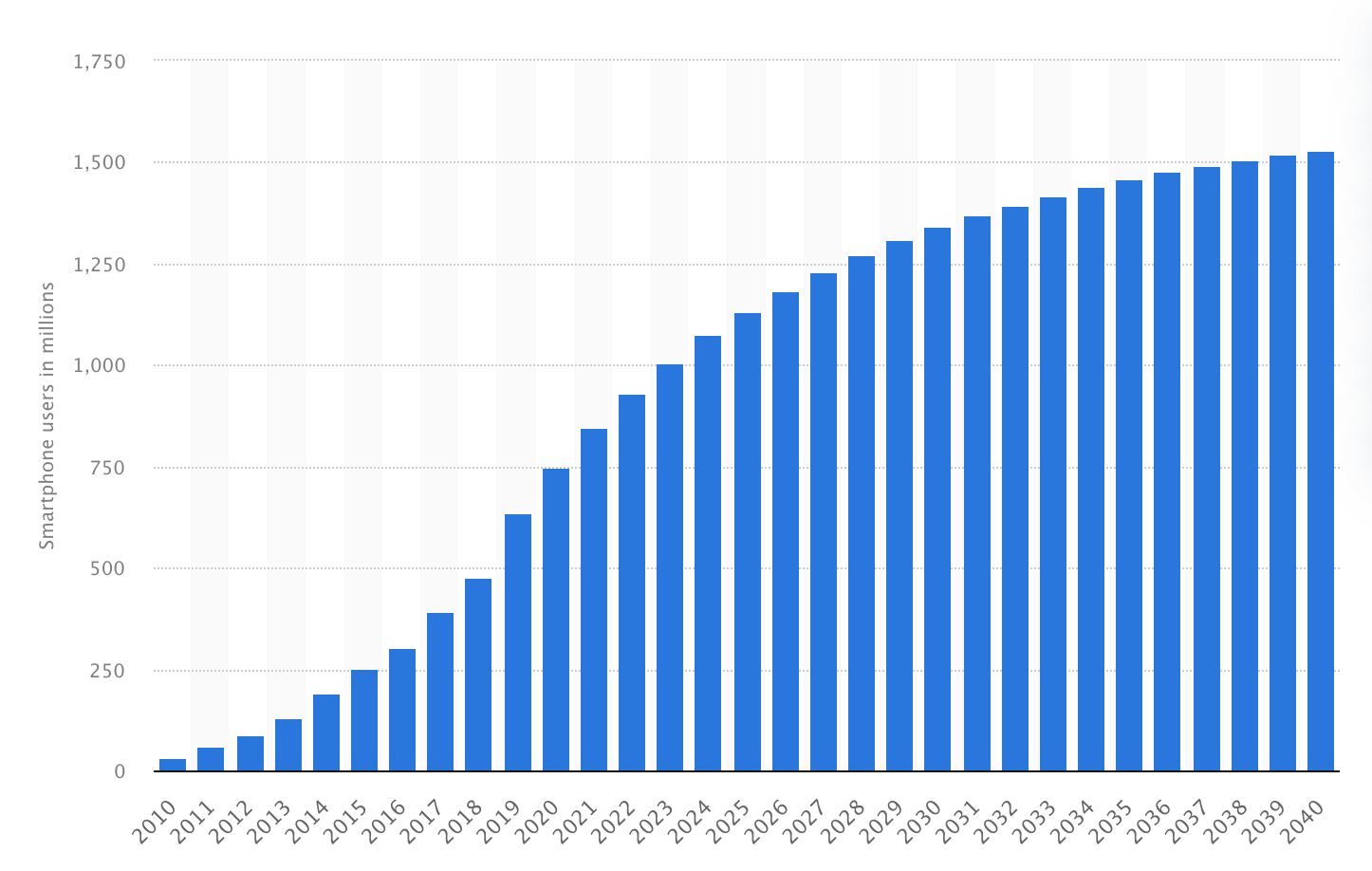

In a recent survey posted by Statista, it was found that in 2012, only 90.63 million people owned at least one smartphone, however 10 years down the line, in 2021, more than 880 million own at least one smartphone and spend a minimum of 3 hours per day on their devices.

The rapid rise in smartphone usage among consumers have enabled them to avail an array of services, right from ordering food and shopping online to availing the services of a personal loan and credit line, right at their fingertips, which has further contributed to the meteoric rise of digital lending in India.

4. Innovative Operating Models

Prior to 2010, the only operating model known to lenders was one where there would be only two stakeholders in the lending value chain, the loan provider and the borrower. However, prior to the introduction and widespread adoption of innovative lending models by fintech, lenders, aggregators and providers, stakeholders are now able to disburse more innovative loans than ever before.

For instance, one of our key offerings, the Finflux Loan Management System, arrives with a co-lending feature, which makes it possible for two or more lenders to seamlessly collaborate with each other, pool in funds and render the borrower any type of loan they require. Along with this, co-lending enables lenders to seamlessly integrate frequently used services and ultimately service the customer better, contributing to better retention of borrowers.

Over and above co-lending, some other innovative models, stakeholders in the lending industry often rely on include.

- Aggregator\ Partnership model

- Independent platform

- Peer-to-peer platform

- “Value +” service in addition to a core service

Observers from the industry have continuously noted that the adoption of these innovative models have served as one of the strongest pillars of growth behind the rapid rise of digital lending in India.

5. Regulatory Environment

Last but not least, regulations and compliance have always been a challenge for stakeholders in the lending industry. If you take into consideration any industry and its subsequent growth, one pertinent factor is the assistance the stakeholders of the industry receive from government authorities in the form of licensing, regulations and compliance agreements and the same is the case for digital lending in India.

Following the trend of established economies like the US, UK and China, the Indian government launched IndiaStack in 2009. A suite of APIs and a sandbox by design, IndiaStack enables stakeholders to stay compliant with regulatory requirements by leveraging modern technology while at the same time making it easier than ever before to reach desired target customers.

Along with this, the Reserve Bank of India has joined hands with financial institutions and technology companies in recent years to not only set up regulatory bodies but also facilitate the creation and piloting of technologies, which further the goal of financial inclusion among the Indian populace.

The Way Ahead

Witnessing the ongoing trend, it is easy to estimate that the way ahead for the digital lending industry in India is as bright as it ever can be. With the industry reaching an estimated net worth of 350 Billion USD by the end of 2023, there has been no better time in history than today.

Thank you for reading, and I will see you in the next one.

The Reference Shelf

- Key Factors Driving Global Growth in Digital Lending [Link]

- Value of digital lending market in India from 2012 to 2018, with forecasts until 2023 [Link]

- What are the factors responsible for the growth of Digital Lending? [Link]

- Number of smartphone users in India in 2010 to 2020, with estimates until 2040 [Link]