On 2nd September 2021, 8 major banks across the country, right from SBI and HDFC to Axis and Federal, joined hands for the second time (post UPI) to initiate the launch of India’s new Account Aggregators.

But what are account aggregators in the first place, and why are their introduction such a big deal?

Let us understand in today’s blog post.

Table of Contents

- Who Is an Account Aggregator?

- What Does an Account Aggregator Do?

- How Does an Account Aggregator Work?

- How Does Account Aggregation Benefit You?

- Conclusion

- Frequently Asked Questions (FAQs)

- The Reference Shelf

Who Is an Account Aggregator?

According to the Reserve Bank of India, Account Aggregators can be understood as non-banking financial institutions who have secured the necessary licenses (under contract) to retrieve and collect financial information about their customers, share them across institutions on a consensual basis and allow customers better control over their financial information.

Pioneered by an inter regulatory body at the RBI, the formation of Account Aggregators has been underway since 2016, and almost all major financial oversight boards across India took part in its formation right from the Insurance Regulatory and Development Authority (IRDA) to the Pension Fund Regulatory and Development Authority (PFRDA), and the Securities and Exchange Board of India (SEBI) to the Financial Stability and Development Council (FSDC).

Drafted with the intention of reducing financial frauds and allowing end consumers better access over their financial information, the RBI at the 2nd September event announced that India would be home to several Account Aggregators, all of whom will be tasked with increasing financial inclusion in the country of 1.3 billion by leveraging modern fintech technology.

What Does an Account Aggregator Do?

Initially conceptualised with the intention of curbing the rising threat of financial fraud, the current version of Account Aggregators allows customers streamlined access to multiple financial institutions under a single portal along with providing them better control over the financial data they want to share with institutions based on a consent method.

In simple terms, the function of an account aggregator can be understood as the facilitation of smooth flow of financial information of customers between institutions.

How Does an Account Aggregator Work?

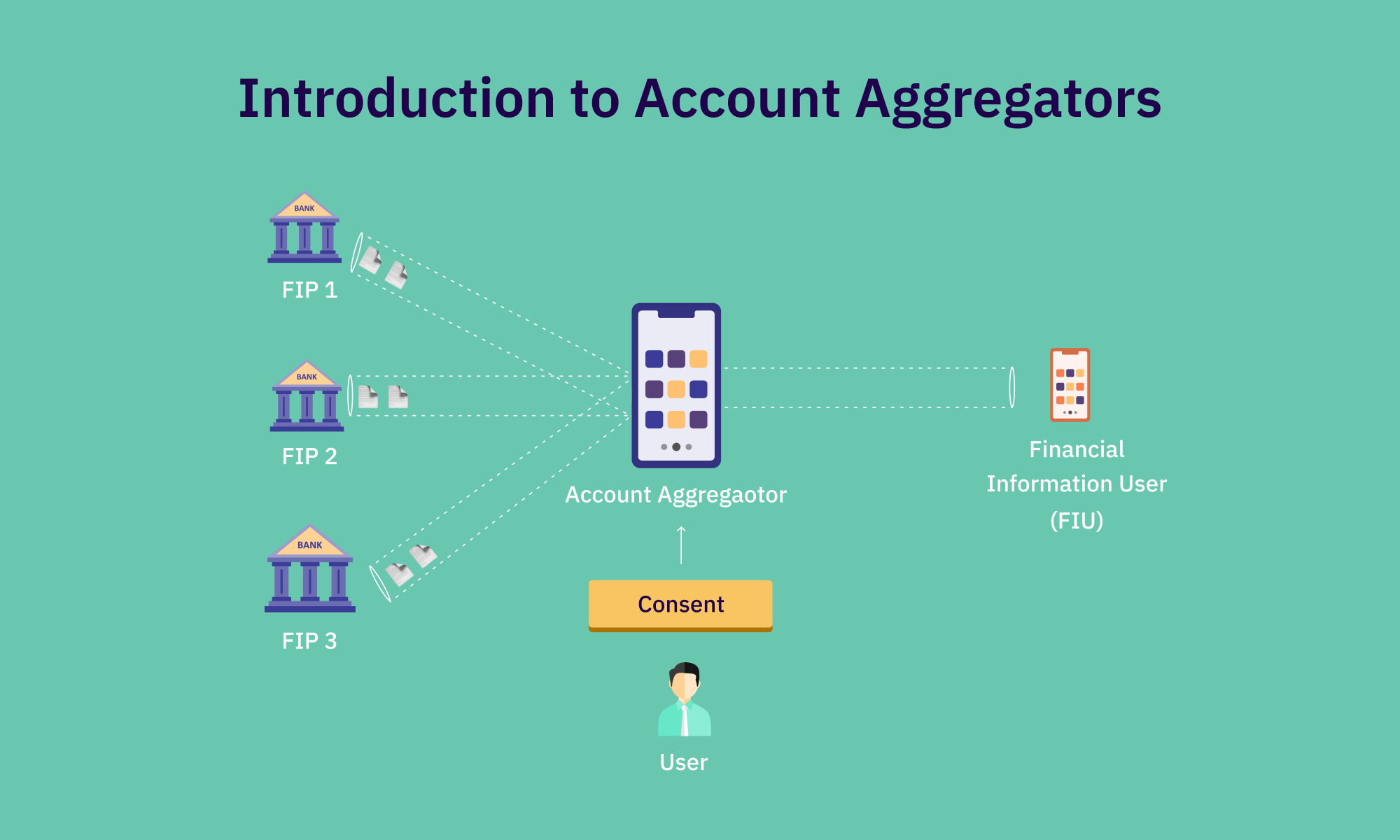

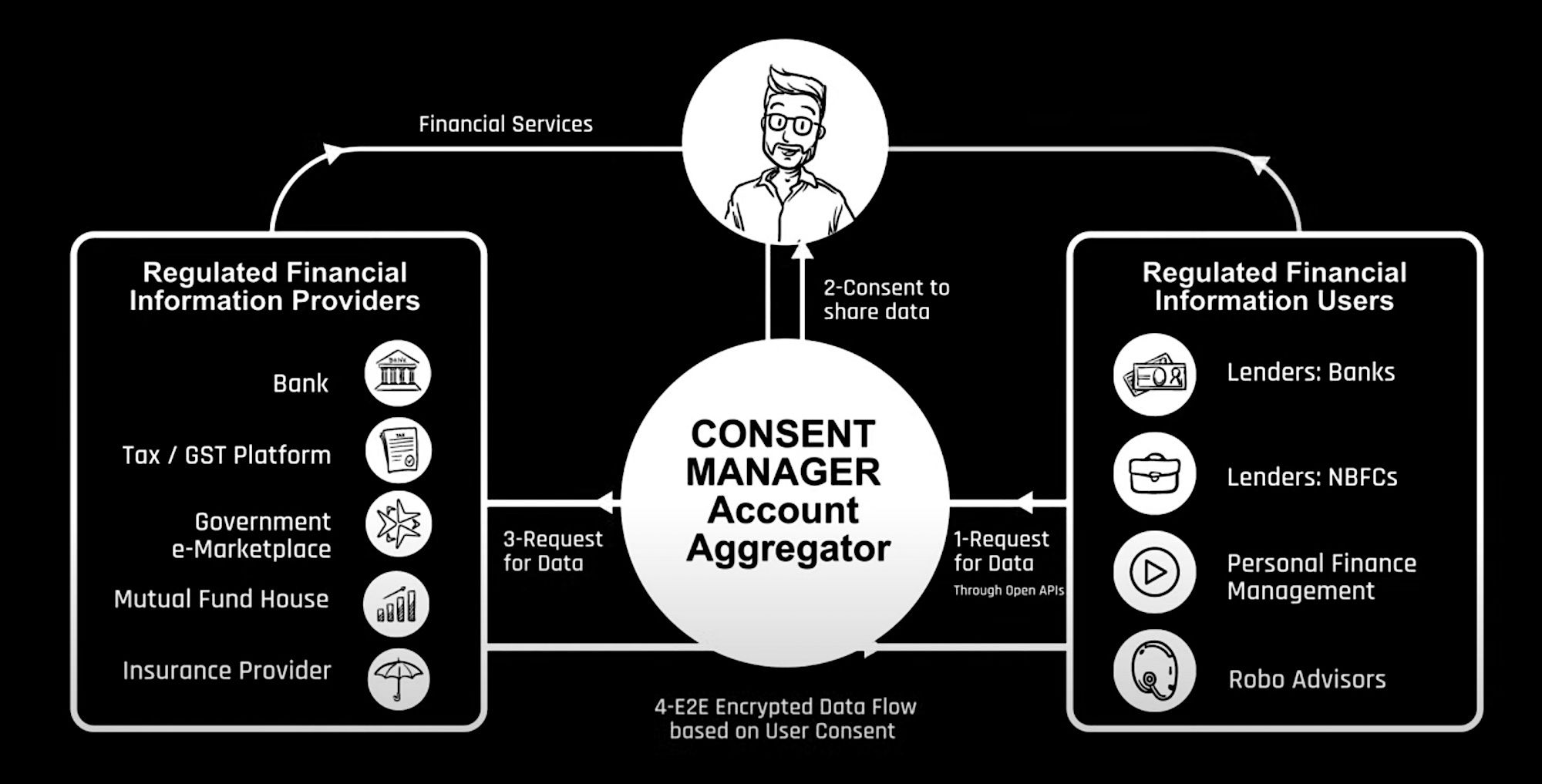

At its core, all account aggregators in India share a three-tier structure.

- FIP (Financial Information Provider)

- Account Aggregator

- FIU (Financial Information User)

A FIP can be any institution, either a banking or non-banking financial institution, which collects and stores the financial information of the customer, such as the income tax department, IRDA, PFRDA or the EPFO. On the other hand, an FIU can be any institution which consumes the data provided by the FIP, and in wide regard, they can be comprised of lending institutions, Robo advisors, personal finance advisors etc.

As illustrated in the graphic below, a regulated financial information provider is responsible for collecting and storing the customer data, and a regulated financial information user is responsible for consuming that provided information such as to assess the eligibility of the end consumer and further the goal of financial inclusion.

At the centre of this arrangement are Account Aggregators who facilitate the smooth flow of information between the FIP and FUP while simultaneously allowing the customer increased control over their data via consent methodologies that is choosing which financial institution the data should be shared with and for how long.

But, How Does Account Aggregation Benefit You?

Now that we understand the essence of account aggregation and their functions, you must be wondering how its deployment advantages you, the end customer.

Right at their inception, account aggregation as a service arrives with several benefits for the end customer, some of the most significant of which are as shared below.

- Reduced Processing Times

If you have ever tried opening a new bank account or made an effort to transfer branches of your existing account, I am sure you too got frustrated with the long queues and extended processing times institutions requested to process simple requests.

Taking this into account, the account aggregation process aims to not only obliterate long queues at customer interaction points but also reduce the processing times required by institutions to fulfil customer requests. By ensuring a smooth flow of information between institutions, you can instantaneously access and share your financial information with authorities, saving both stakeholders time and money.

2. Increased Control Over Data

Long before the introduction of account aggregators, financial and non-banking financial institutions practised the skill of collecting and storing confidential financial information of customers, and in the absence of any oversight authority, these institutions often acted as owners of this information, rather than custodians and often customers had no way of accessing this data for themselves.

However, with the introduction of account aggregators, the RBI aims to change that by empowering the end consumer with increased access and control over their financial information right from deciding whom to share the data with and for what tenure, to taking a call on which data can be assessed and which ones must be kept confidential.

This initiative not only transfers the information ownerships to its rightful custodians but also aims to ease the process of abiding by future data privacy and security regulations.

3. Increased Financial Inclusion

Last but not least, financial institutions across the country, namely FIPs, can now have streamlined access to a wealth of customer financial information, which can not only be used to identify the right target customers but also instantaneously verify their eligibility for financial instruments, thereby furthering the goal of financial inclusion.

To put these into context, let’s understand the impact of these advantages with an example.

Assume that you are a young working professional at an MNC (age 24 years), and you draw a monthly in hand income of ₹50,000. Prior to this, you worked as a freelancer, and although your income was at par, you struggled to get approved for loans, credit cards and other financial instruments due to a lack of synergy between financial institutions and a disproportionate flow of information.

However, now that account aggregation has been introduced, you can not only seamless access all your financial information from FUPs (bank, income tax department, IRDA etc.) but also share it with lenders at the tap of a finger. You have the option of deciding which data points you would like shared, plus how long the FIU (lenders, personal finance assistant, Robo advisor) will have access to the data.

Thus, now at the tap of a few buttons, you can share your past 3 years ITR reports with your lender, along with the current investment summary from CAMS, insurance investments from IRDA and idle cash from your banking partner. Assessing all these data, your lender can instantaneously verify your eligibility for a loan (both large and small ticket) as they now have access to wider eligibility checks, and once you are approved, you can withdraw the FIUs access from the data.

In the end, you gain complete control over your data and instantly get approved for a loan or a credit card, for which you needed to struggle earlier.

In Conclusion

The RBI and FSDC are hailing the launch of account aggregators in India as a massive success, and we at Finflux are too of the opinion that the conceptualization of such a service truly arrives with the potential of redefining the future of financial services in India for days to come.

As Infosys chairman Nandan Nilekani rightly noted at the launch event, “We can confidently say that there is no other country in the world that has built a robust infrastructure at this scale where its people can leverage their data; […] empowered by consumers using their own data, enables a huge amount of credit to small businesses. It can lead to the democratisation of credit.”

Thank you for reading, and I will see you in the next one.

Frequently Asked Questions (FAQs)

- What Is Account Aggregation?

Account aggregation in simple terms is the process of ensuring a smooth flow of your financial information between financial and non-banking financial institutions, and allowing you better control over who has access to the data and for what tenure.

2. How Does Account Aggregation Work?

Account aggregation works by first collecting all your financial information from FIPs, then assessing and encrypting them, followed by sharing them with FUPs upon your consent and approval.

3. Is Account Aggregation Safe?

As of the moment the RBI and FSDC claim that the account aggregation process is completely safe as it leverages modern fintech technology to deter cyberattacks, privacy and fraud violations, however the real extent of these claims can only be realized in the upcoming days.