If you are an MSME owner in India, I am sure that one of the struggles you face on a regular basis is getting access to affordable credit to expand and continue your business operations. Likewise, if you are a lender in India, chances are, you have experienced struggle in processing requests for small business loans. Luckily for both of you, the lending industry in India is about to change for the better, and in today’s blog post, we will share with you a snapshot of the future.

Without further ado, let’s get started.

Table of Contents

- Introducing OCEN

- How Does the OCEN Framework Work?

- Pain Points OCEN Is Solving

- The Way Ahead

- Frequently Asked Questions [FAQs]

- The Reference Shelf

Introducing OCEN

On 24th July 2020, Nandan Nilekani, co-founder of Infosys, announced the launch of OCEN, a disruptive architecture designed to advance credit inclusion in India. The industry acronym for Open Credit Enablement Network, OCEN, aims to increase credit access in India by collaborating with the recently launched account aggregator framework.

But what exactly is OCEN, and why is its launch being hailed as the next disruptive innovation of the Indian lending industry?

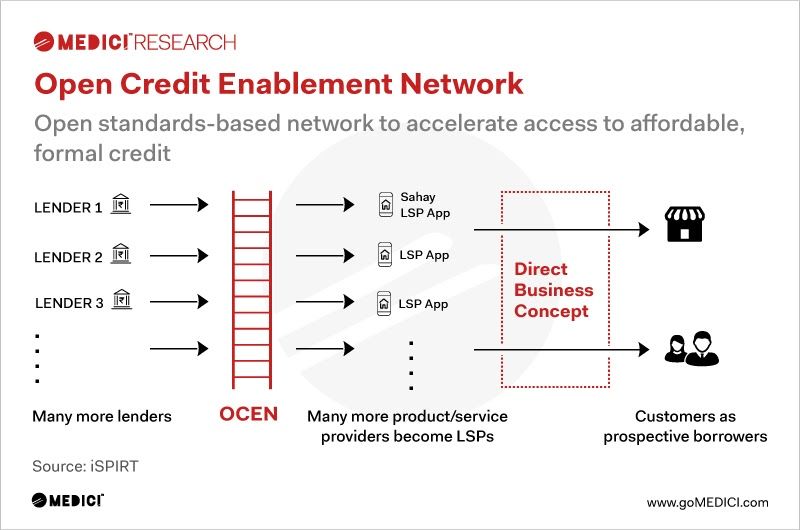

In simple terms, OCEN can be understood as a software architecture which brings together various stakeholders of the lending ecosystem under one roof by leveraging APIs and smart integrations, thereby allowing lenders to craft customized credit instruments and businesses streamlined access to a marketplace which hosts a wide range of lending products.

As illustrated in the graphic below, OCEN is a framework of APIs which allows for seamless interaction between lenders, loan service providers (LSPs) and account aggregators.

At present, the business lending ecosystem in India primarily tends to the formal sector and approximately serves 50 million customers a year; however, with the launch of this platform, the innovators (IndiaStack) are aiming at serving the next billion. In order to understand this better, let’s take the help of an example.

Imagine you are the owner of a small business in India, which is registered under both the MSME scheme as well as the Good and Service Tax (GST) department. As a small business, you have a yearly turnover of approximately ₹700,000; however, due to the onset of an opportunity, you now want to leverage a business loan and expand your operations.

Despite having all your papers in order, when you approach a bank or a non-banking financial institution (NBFC), you are denied a loan on the grounds that the institution doesn’t deal in small ticket lending instruments.

But the same institution caters to more established business owners due to the simple reason that they can apply for high ticket loans and thus are profitable customers of the bank.

In simple terms, since you are a small business owner, processing your request for a small ticket loan is an expensive and time-consuming affair for the bank or NBFC, and thus they deny your request.

This is the exact situation the OCEN framework aims to change by bringing together more than 30 stakeholders from the lending industry by acting as a common language to connect lenders and loan service providers (LSPs) to more than 300 million untapped customers in India via the facilitation of a unique marketplace.

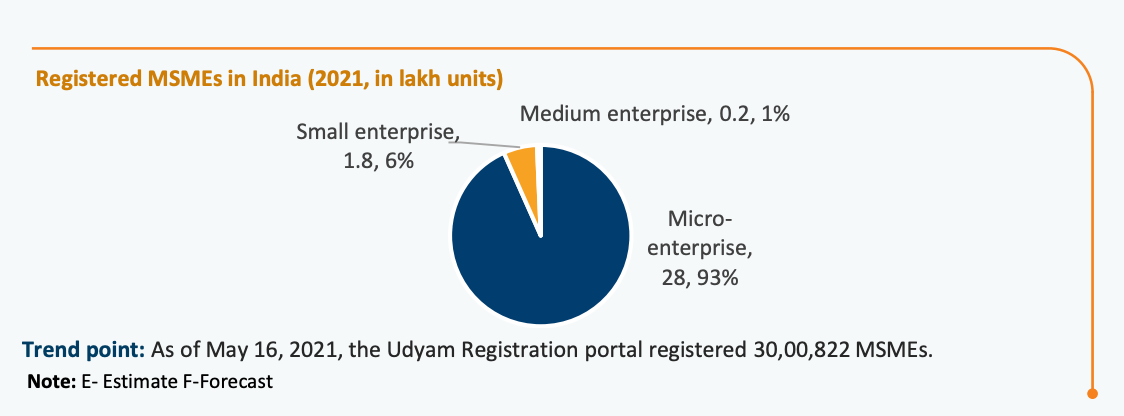

As per a May 2021 report by the IBEF (India Brand Equity Foundation) and Ministry of MSMEs, at present, there are 3 million registered MSMEs in the country, and more than 93% of these entities are micro-businesses meaning they have less than ₹5 crores of annual turnover. Along with this, as per a 2020 Statista report, India is home to more than 63 million MSMEs, meaning more than 95% of the businesses in India are not registered.

While at first glance it might appear that being an unregistered business is not concerning, in reality, an unregistered business suffers from a series of disadvantages, with one of the most significant of them being no access to formal credit instruments, and in the next 2 years, the OCEN framework aims to challenge this situation and bring a majority of businesses in India under the radar of formal credit.

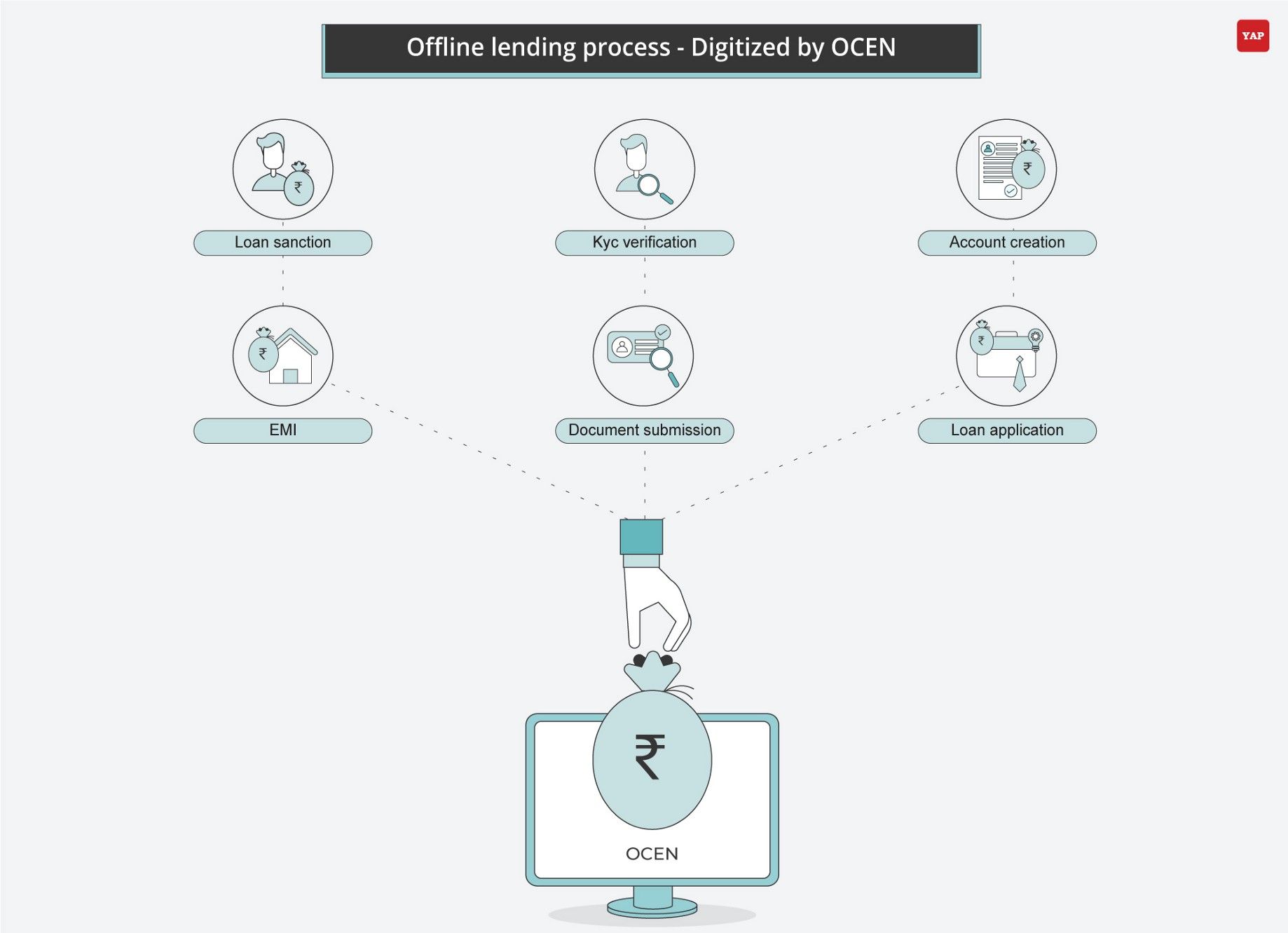

How Does the OCEN Framework Work?

While the exact mechanics of the OCEN framework are not completely clear, Nandan Nilekani explained at a virtual event that the OCEN framework would provide key stakeholders with a standard set of tools such that the typical components of a lending value chain can be more effectively managed.

Right from acting as a mediator between Fintechs and eCommerce players to more standard lending institutions such as SCBs (Standard Commercial Banks), the OCEN credit rails allows for the development of innovative financial credit products at scale.

At present, the current rendition of the framework dubbed Sahay is ready for invoice discounting, and within the next 2 years, the team at IndiaStack, along with other key stakeholders, aims to expand the system such that even kirana shop owners are able to seamlessly apply for an intraday loan through the comfort of their smartphone, simply by sharing their transacting history.

As of date, more than 30 participants, right from neo banks and khata book companies to tax filing applications and well-known lenders such as SBI and IDFC, are running a pilot to test out the technology.

Pain Points OCEN Is Solving

While the real impact of this groundbreaking technology is yet to be realized, shared below are some of the most significant pain points OCEN is addressing in the Indian lending industry as of today.

- Streamlined identification of creditworthy borrowers

- Reducing the cost of acquiring new borrowers

- Automating integrations between lenders and marketplaces

- Reducing loan deposit turnaround time

- Simplifying the creation of custom credit instruments

- Increasing credit access among MSME borrowers across India

The Way Ahead

Once the OCEN framework is fully operational, the innovators expect to introduce 1 billion customers into India’s formal credit network by leveraging this technology, and past integrations across BNPL-FinTech partnerships demonstrate the potential of technology.

As the Indian lending ecosystem continues to grow at a rapid pace, observers and key stakeholders continue to maintain that technologies which foster collaboration, such as OCEN and Account Aggregation, will play a major role in democratizating credit for the next generation of Indian borrowers.

Thank you for reading, and I will see you in the next one.

Frequently Asked Questions [FAQs]

- What Is Open Credit Enablement Network (OCEN)?

Open Credit Enablement Network (OCEN) can be understood as a standard set of tools which leverage Open APIs and smart integrations to increase the efficiency of the lending value. It is primarily used by LSPs (Loan Service Providers) and Lenders such that they can craft customized credit offerings for customers and increase credit inclusion in India.

2. How Does Open Credit Enablement Network (OCEN) Work?

Open Credit Enablement Network (OCEN) works by integrating and automating various manual processes involved in the lending value chain, such as identification of credit worthy customers, onboarding new borrowers, thereby decreasing their overall operational cost and increasing efficiency.

3. What Pain Points is Open Credit Enablement Network (OCEN) Solving?

Open Credit Enablement Network (OCEN) is solving a number of pain points currently present in the Indian lending ecosystem and you can read them here.

4. What Is My Benefit from Open Credit Enablement Network (OCEN)?

Once the Open Credit Enablement Network (OCEN) is fully implemented, as an MSME business owner you can access a wider pool of both small and high ticket loans, via an innovative marketplace. Additionally, lenders will be able to craft customized credit instruments to fulfil your unique requirements at a lower cost, thus making the entire process of borrowing as an MSME in India more affordable.

5. Who Developed Open Credit Enablement Network (OCEN)?

Open Credit Enablement Network (OCEN) was developed by the team at IndiaStack, and you can read about them here.

6. When Will Open Credit Enablement Network (OCEN) Launch PAN India?

The first deployment of the Open Credit Enablement Network (OCEN) was expected in September, 2020, but as of recent news final deployment might occur in Q1, 2021.

The Reference Shelf

- iSPIRT Second Open House on OCEN: Varied LSP Possibilities [Link]

- India’s Open Credit Enablement Network (OCEN) [Link]

- Open Credit Enablement Network to launch through ‘Sahay’ app by September [Link]

- Open Credit Enablement Network to disrupt lending infrastructure [Link]

- Open Credit Enablement Network (OCEN) [Link]

- Open credit enablement network will democratise credit: Nandan Nilekani [Link]

- MSME Industry in India [Link]

- Digital Lending — Open Credit Enablement Network [Link]