The microfinance industry has been witnessing stellar growth over the last decade. The sector grew 16.5 times, from ₹ 17 thousand crore in 2012 to ₹ 2.85 lakh crore in 2022[1]. With a market share of 37.53 %[2], NBFC-MFIs stand as the leading financial provider in this sector.

Thanks to the proven model of Joint Liability Groups (JLGs), the Microfinance Institutions (MFIs) witnessed phenomenal growth in the past decade. This model enabled doorstep access of financial services to the underserved population, mainly women.

In addition to the JLG model, the Government of India initiatives listed below have also aided the growth of MFIs.

• Pradhan Mantri Jan-Dhan Yojana (PMJDY) – This government scheme was the primary reason for millions of Indians to have a bank account [3].

• Jan-Dhan Aadhaar-Mobile (JAM) trinity – Helps Indians to link their Jan Dhan account, Aadhaar card, and Mobile number.

• India Stack – Comprises of paperless, cashless, and consent layers that help lenders to collaborate with Fintechs and create products based on customer needs.

• Aadhaar Penetration – Aided the shift of the traditional banking system to a digital model for enabling technology players with electronic Know Your Customer (eKYC) and authentication services.

Challenges Amid Growth:

The above factors are accelerating the microfinance penetration. But the industry is witnessing cracks due to the challenges in the current model of borrower engagement – the High Touch Model (HTM).

In contrast to the Low-Touch Model (LTM), the HTM has high engagement level between the loan officer and the borrower. This may look encouraging from an aerial view. But this model is one of the main reasons for the high attrition rate of the loan officers and the increase in Operational Expenses (OPEX). According to a KPMG report by MFIN[4], this model does not offer borrowers the necessary value proposition to attend group meetings and maintain group dynamics post-adoption of the cashless collections.

This led the microfinance players to move towards a more efficient model – the Tech-Touch Model (TTM).

Tech-Touch Model – Amalgamation of Low-Touch and High-Touch Models

The Tech-Touch Model strikes a perfect balance between the efficiency and cost savings of a low-touch model and the personalization and support that high-touch model offers. In addition, it is an advanced version, extending the best of both worlds – automation and self-service tools from the low-touch model and customer engagement from the high-touch model.

Many MFIs are gradually adopting the tech-touch model to digitize their loan sourcing, management, and collection processes. By leveraging the benefits of the TTM, lenders are on the path to Digital Microfinance.

What does Digital Microfinance Entail?

Digital Microfinance is the hot, new buzzword in the microfinance realm. As the name suggests, it is the use of digital technologies to disburse micro loans to low-income individuals.

With TTM at its core, digital microfinance can digitize, automate, and streamline the loan processes such as loan disbursement, loan management, and collections. By digitizing these processes, MFIs can significantly reduce the time and cost associated with traditional loan origination methods.

Usually, loan sourcing is the primary step before loan origination. First, the loan officer responsible for loan sourcing goes to the self-help groups and collects the borrower’s details. Then, he collects all the requisite borrower information and takes it to the branch office, consolidates the borrower details, and assesses the borrower’s creditworthiness. All these steps can take up to 3 days. Not to forget the vast volume of paperwork they handle.

It can be seen that the conventional way of loan sourcing can be time-consuming and inconvenient. That is why it is crucial for MFIs to opt for digital methods and start exercising digital microfinance.

Digital Microfinance – Road to Productive & Effective Loan Originations

Loan origination is a critical process for lenders. From initial credit assessment, approving/denying loan applications, to disbursing the right loan amount to the right borrower, loan origination can be quite tricky. It is even trickier to originate accurate loans in a matter of minutes/seconds.

Digital Microfinance accelerates loan originations by employing digital methods for KYC verification, bank account verification, borrower credibility check, borrower credit assessment, performing Compulsory Group Training, etc.

Expedite Loan Sourcing via Digitization

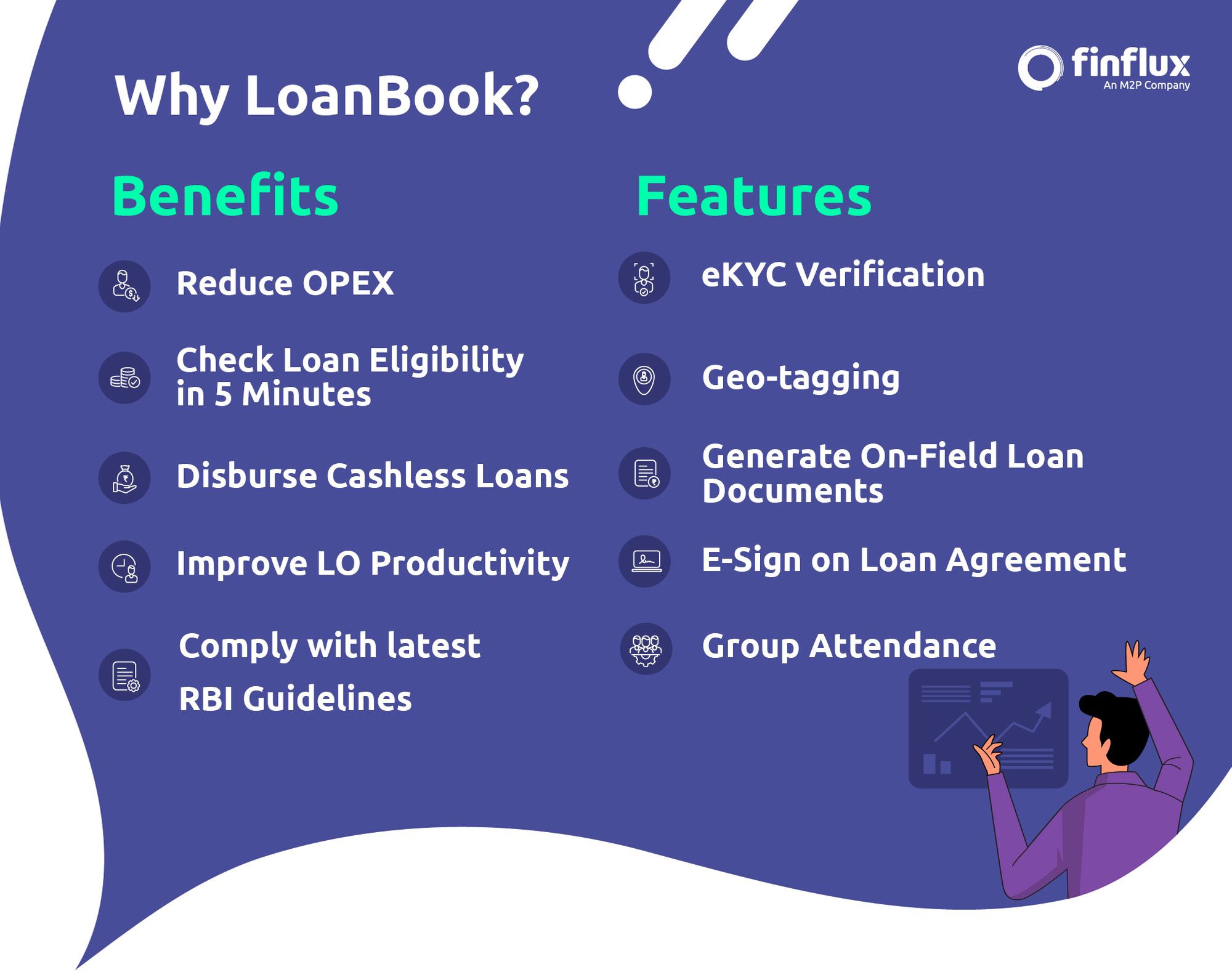

With digital tools like Finflux’s LoanBook application, loan sourcing becomes a piece of cake for the loan officers.

Here’s how.

The LoanBook application comprehensively digitizes all the work carried out by the loan officer, starting from loan sourcing to management and collections.

Using the application, the loan officer adds every member of the JLG into the system along with their details. After entering the basic information, the officer can verify the borrower’s details.

In loan origination, the LoanBook application can help the MFIs expedite the following:

✔ Ekyc Verification

Ekyc verification for the borrower can be done either by validating their fingerprint or through OTP verification or Iris scan.

✔ Penny Drop Verification

The credibility of the borrower’s bank account is verified by dropping a penny into their bank account.

✔ Geo-tagging

At the time of sourcing, the field officers can use this feature to tag the location of the borrowers and the self-help groups (where center meetings are conducted). Geo-tagging also eases the loan collection process by quickly pointing to the borrower’s location.

After completing eKYC, the loan officer adds the details of the borrower’s family members and specifies the loan amount required by the borrower. This is where Finflux’s inbuilt Embedded Business Rule Engine (BRE) comes into the picture.

With Finflux, the time taken for loan decisions reduces to 3 minutes from 3 days.

Many enterprise MFIs are working closely with Finflux and are already on the road to Digital Microfinance. They have simplified their loan origination process, reduced the TurnAround Time (TAT) from weeks to days, and mitigated their OPEX. These MFIs have unlocked a new model for optimizing their loan sourcing process, scaling their profitability, and increasing financial access to women in rural and underserved markets.

This is what our client – Pragati Finserv has to say about us:

Do you want to originate faster loans?

Schedule a demo with us.

References:

[1] – Microfinance Industry Growth

[2] – NBFCs overtook banks in market share

[3] – Press Release