Do you know?

Only 25% to 30% of loans employ full automation[1] when it comes to credit decisions.

Yes, the road to full automation is long and exhausting due to barriers such as extensive reliance on legacy systems, a lack of technological capabilities, dependency on manual processes, etc.

But, when implemented, full automation can help the lender in:

· Reducing underwriting costs and credit decisioning time

· Processing huge volumes of loan applications seamlessly

· Ensuring error-free loan approvals

And finally, it helps in offering a personalized customer experience and ultimately reducing credit losses.

Now that we have evinced the need for fully automated credit decisions, let’s dive into the ‘how.’

Business Rule Engine – Leveraging the Power of Automation

Using a Business Rule Engine (BRE) to automate the underwriting and credit decisioning processes, lenders can quickly and accurately originate cost-effective, configurable, and scalable loans. Further, it not only helps the lender with cutting-edge technology, but it also originates error-free loans with minimal manual intervention.

What exactly is a BRE?

A Business Rule Engine is a software application that considers various factors and parameters to make a complicated business decision in seconds. By accepting inputs from many sources, the BRE makes it easier for lenders to arrive at actionable business decisions accurately.

In this case, loan origination.

Every lender has a secret recipe (credit policy) for their loan origination process. The credit policy can be exhaustive, consisting of hundreds (sometimes thousands) of parameters. Irrespective of the number of parameters involved in a credit decisioning process, a lender can effortlessly configure the BRE and devise a hyper-personalized plan specific to the borrower.

Finflux’s BRE is one such engine that can automate the entire loan origination process, starting from pre-qualification to underwriting and credit decisioning. Being an embedded BRE specific to lending, Finflux’s engine gives a competitive edge over any third-party BRE. Unlike a third-party BRE, which requires lenders to build the credit policy from the ground up, Finflux BRE has pre-built templates and parameters for smooth configuration.

Underwriting

Finflux’s BRE eliminates the need for manual underwriting by reducing the underwriting time to milliseconds, no matter the volume of applications.

Workflow Decisioning

Each borrower application is unique in itself. If there are ‘n’ business steps involved in a credit decisioning process, not all the applications will pass through all the steps. Depending on the borrower’s portfolio and the lender’s policy, the application can be routed in different ways. A lender can ensure that the application is processed only through the necessary steps in this manner.

Lead Qualification

Borrowers apply for loans through various channels such as bank websites, mobile applications, field officers, etc. Nevertheless, not all borrowers are potential leads. A few would drop in to enquire about the loans. Finflux BRE’s machine-aided decisioning helps the lender differentiate the prospects from the standard enquires by running a simple eligibility check.

Pricing Suggestion & Charge Calculation

When a borrower applies for a loan, the BRE runs a thorough assessment of their portfolio and suggests the loan eligibility, repayment cycle, interest rates, tenure, and the entire EMI package to the borrower. The pricing suggestion and charge calculation are borrower-specific.

Configuring a BRE:

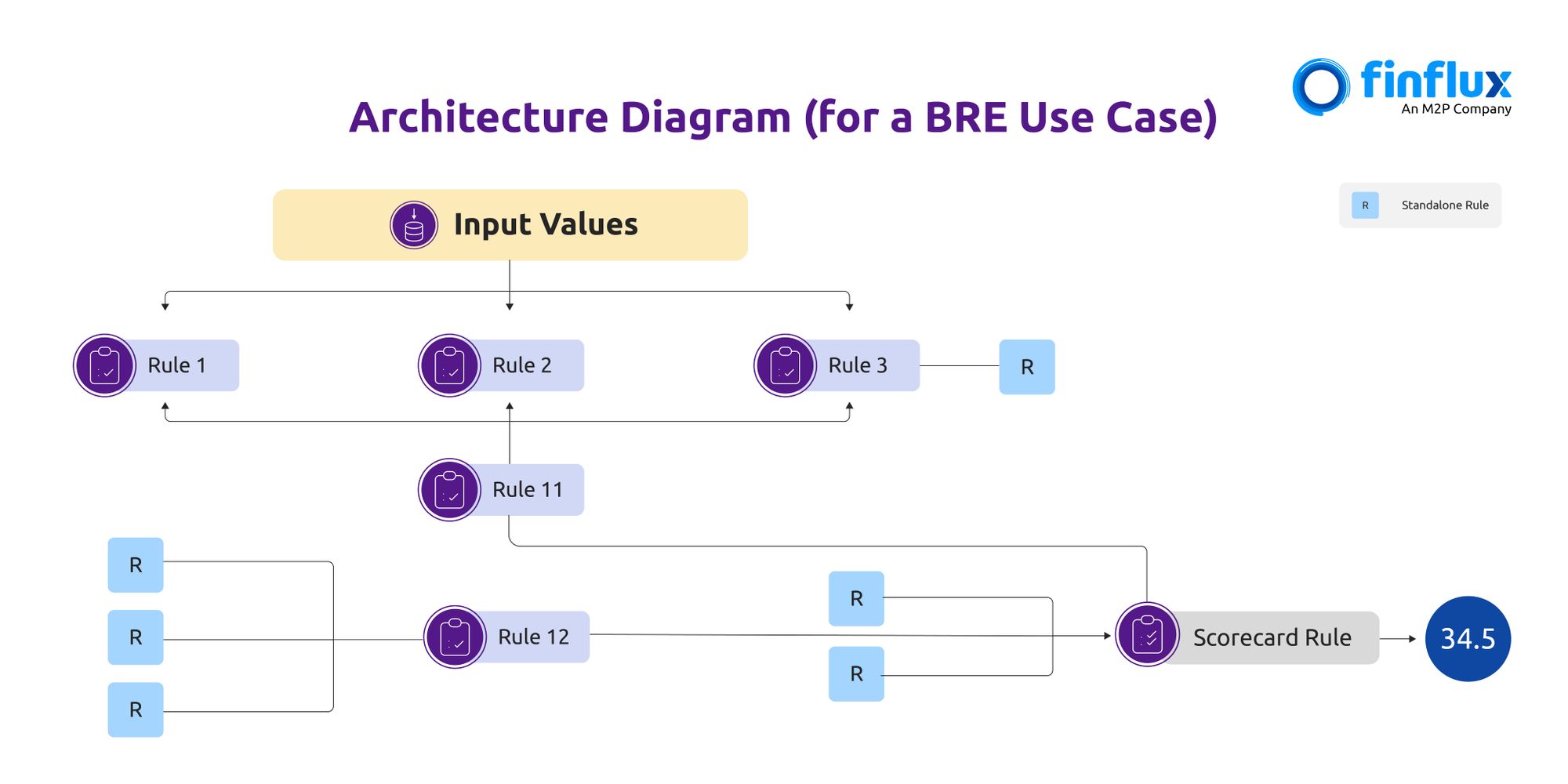

A lender can configure all the use cases using the Graph Rule model in the BRE. The architecture diagram consists of input values, rules, the interaction between the rules, and the output parameters in general.

The entire configuration process is simple, neat, involves no code, and can be implemented by anyone with basic computer skills. The drag-and-drop feature of the BRE model eases the relationship between various rules.

The above diagram shows the use case for creating a borrower scorecard based on various parameters and rules. This scorecard gives a score out of 50 to define the borrower’s creditworthiness.

A lender can configure the BRE with any number of requisite use cases based on their standard policies.

BRE Walkthrough

This walkthrough takes a simple use case and explains the steps involved in setting up the input/output parameters, defining a logic, and testing the use case using different inputs.

Now that the BRE is configured, the use cases must be tested in different ways before it is deployed in real-time.

Testing mechanisms:

Testing the BRE for various use cases ensures seamless loan origination. Using the testing mechanisms, the lender can compare the existing and new workflows and experiment with the BRE to improve the credit policy using multiple tests.

Here are the 3 types of testing mechanisms that come with Finflux BRE.

· Back Testing – Testing a new BRE with existing data with reports generated from existing and new BRE.

· A/B Testing – Creating a new version of the existing BRE and routing 100% of the use cases through both BREs.

· Champion Challenger – Routing 50% of the use cases to the existing BRE and the remaining use cases to the newly configured BRE.

Finflux’s Business Rule Engine (BRE) is a must-have for lenders looking to automate their loan origination process. The Finflux team has extensive experience working with multiple lenders, and they understand the unique challenges faced by them. As a result, they have tailor-made the engine to address the specific needs of the lenders.

Contact Finflux today and Schedule a free demo.

Notes:

[1] Average percentage of loans that employs full automation – Experian study on Credit Decisioning and Alternative Data Use.