In the midst of the COVID-19 pandemic, when almost every industry across India was witnessing a sharp downturn in its growth trajectory, the Indian microfinance industry developed a significant amount of resilience and was able to not only sustain itself but also register a massive growth of 31% in FY20, by jumping its loan portfolio to ₹2.36 lakh crores.

While this number might appear to be astounding at first glance, in reality, the Indian microfinance industry has been steadily growing over the past decade, and a recent research by Dr Swati Sharma of Amity Business School, Rajasthan, highlighted this fact.

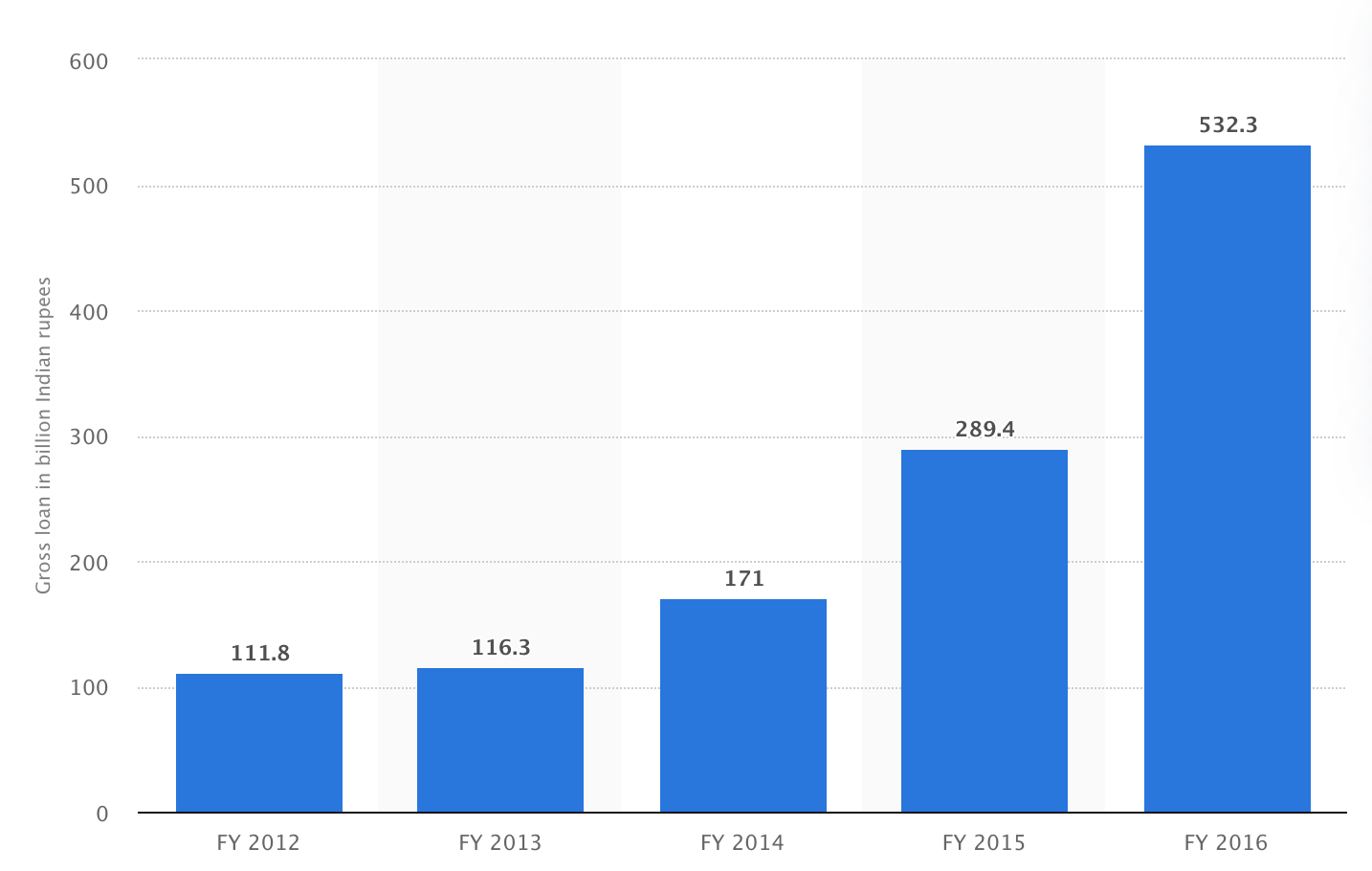

Along with this, a quick look at the recent Statista report outlines the consistent growth the Indian microfinance industry has witnessed over the period of FY12-FY16, and all these reports go on to establish the fact, that not only is microfinance being widely accepted by the Indian populace but also demand for their services is constantly on the rise, making the proposition of starting a microfinance business in India even more attractive.

But, how can you start a microfinance business in India?

That is exactly what we will be talking about in today’s blog post, so without further ado, let’s get started.

Table of Contents

- What Is a Microfinance Institution?

- Forming a Microfinance Company in India

- Registering a Microfinance Business as an NBFC

- Registering a Microfinance Business Under Section 8

- In Conclusion

What Is a Microfinance Institution?

Before we learn how you can start a microfinance business in India, one of the most important aspects we need to invest our attention to is understanding the meaning of a microfinance company.

As per the RBI (Reserve Bank of India), microfinance or microfinance institutions can be defined as being financial institutions, which extend financial instruments such as small-ticket loans to the underbanked, low-income and weaker sections of the economy.

Primarily developed with the intention of increasing financial inclusion by providing the weaker sections of the economy an affordable and easily accessible tool to rise out of poverty, microfinance in today’s India provides its benefactors with a number of advantages such as:

- Providing easy and affordable access to credit instruments to the weaker sections of the society by leveraging group lending and thus fostering a joint liability mechanism among the benefactors such that on-time repayment can be seamlessly achieved.

- Providing easy and trustworthy access to traditional financial instruments such as saving bank accounts, such that financial inclusion can be raised among the poor.

- Ousting the use and increasing reliance of the poor on moneylenders and informal credit instruments, which are infamous for charging exorbitant rates of interest, and instead providing them access to affordable credit without the requirement of guarantors and assets or collaterals.

Starting a Microfinance Business in India

Now that you understand the meaning of a microfinance institution and the advantages it extends to its benefactors let us understand how you can start a microfinance business in India.

In India, there are two main ways of starting a microfinance business.

- Start an NBFC (non-banking financial institution), which is duly registered with the RBI.

- Register your microfinance business as a Section 8 company under the Section 8 of the Indian Companies Act, 2013.

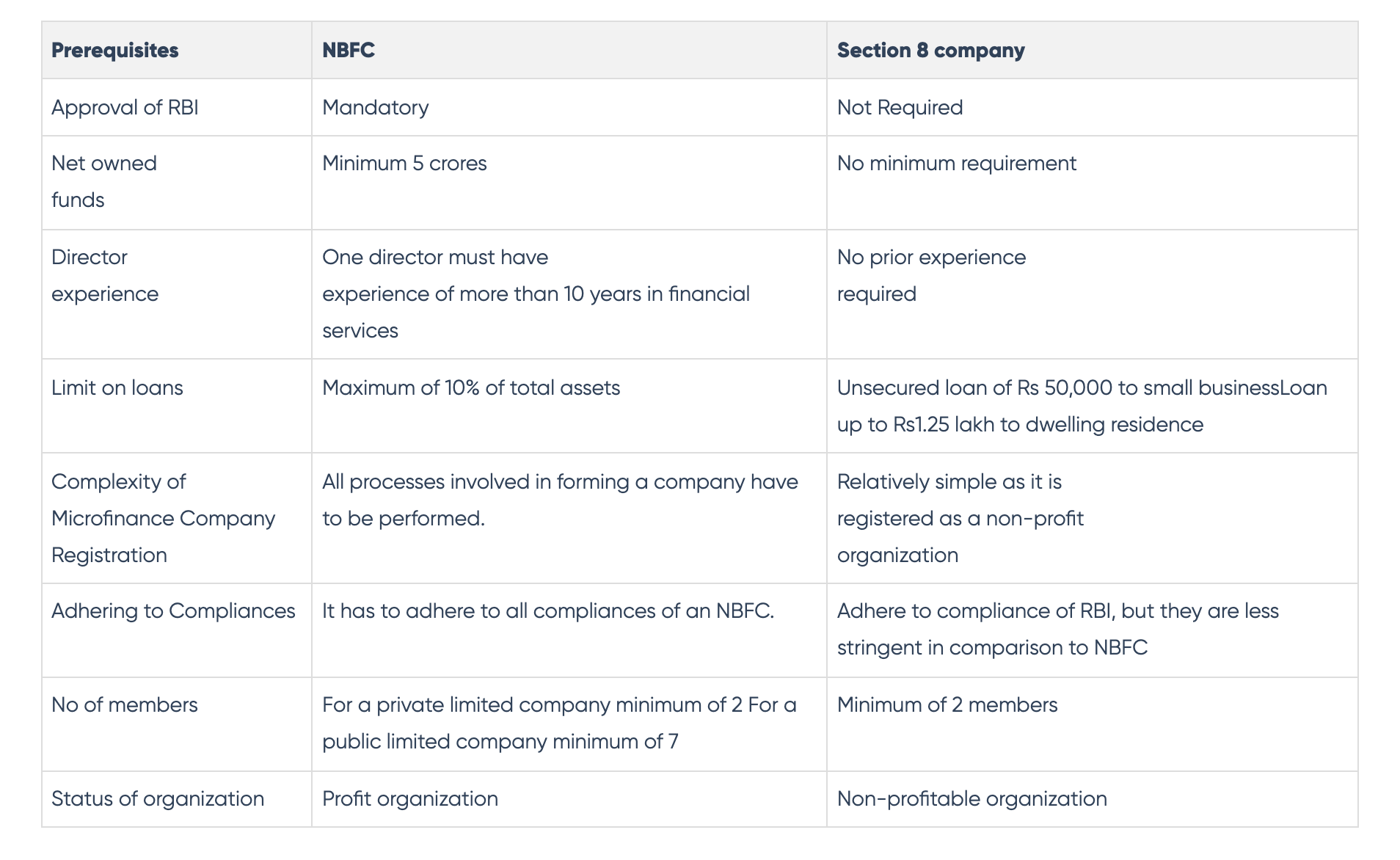

In either of the pathways you follow to start a microfinance business, there are a number of government outlined prerequisites you will need to follow. Some of the most significant of them are as shared below.

Registering a Microfinance Business as an NBFC

Now that you are aware of the prerequisites you need to fulfil in order to start a microfinance business in India, shared below is a rundown of the steps you need to follow in order to register it as an NBFC with the RBI.

- Register Your Company

In order to register your microfinance business as an NBFC, you will first need to form a private or a public limited company. In order to register as a private limited company, you will need to have at least two members present and a paid-up capital of ₹1 lakh, while on the other hand, if you want to start a public limited company, you will need to have at least 7 members and a minimum paid-up capital of ₹5 lakhs.

2. Raise Capital

Once you have registered your microfinance business as an NBFC, the next step of the process is to raise your capital. In the case of a microfinance business registered within India, you will need to raise a capital of ₹5 crores; however, if your company is registered within the northeastern territories of India, you will need to raise a capital of only ₹2 crores.

3. Deposit Your Capital

Once you have secured the capital amount of either ₹5 crores or ₹2 crores as applicable in your case, you will need to deposit the same with an SCB (Scheduled Commercial Bank) in the form of an FD (Fixed Deposit) and acquire a “No Lien” certificate against the same.

4. Submit Your Application

Once you have secured a “No Lien” certificate against your FD, the next step of the process is to submit your application along with your documents to the RBI. At the initial stage, you will need to fill out an online application on the RBI’s website, and post that; you will need to submit a hard copy of your application along with your newly issued licence and other certified documents with the local branch of the RBI.

Some of the most significant documents you will need in order to proceed with your application are as follows.

- Articles of Association and Memorandum of Association from your company registration.

- Incorporation certificate of your company

- A copy of your board resolution document

- A certified copy of your Fixed Deposit receipt from your auditor

- A banker’s certificate stating the net deposited fund along with the “No Lien” certificate

- Banker’s report of your company along with recent credit reports of all your directors

- Net-worth certificates of all your directors duly verified by your auditor along with the educational and professional qualifications of your directors.

- KYC and income proof of your directors

- Proof of past working experience in the financial sector, and

- Structural plan for your microfinance business

Submit all these documents with the duly registered authorities, and post additional clarifications, you will have your microfinance license from the RBI in a matter of few days.

Registering a Microfinance Business Under Section 8

Another pathway to register your microfinance business in India is by registering it under the Section 8 of the Indian Companies Act, 2013. In order to achieve the same, you will need to follow the below-outlined steps.

- Apply for DSC and DIN

The first step in order to register your microfinance business under Section 8 of the Indian Companies Act, 2013 is to apply for a DSC (Digital Signature Certificate) followed by a DIN (Director Identification Number). The idea behind this simply being, both these documents are crucial for approving all the e-forms you will be completing in the upcoming steps.

2. Company Name Approval

As the director of your microfinance business, once you have secured your DIN and DSC, the next step of the process is to seek name approval for your business by filling out the INC-1 form. As per the mandates prescribed by the Section 8 of the Companies Act, 2013, in order to register a microfinance business under this section, your company must contain a combination of the words, “Sanstha”, “Foundation”, or “Micro-Credit.”

3. File for Your MOA and AOA

Once you have secured the approval for your company name, the next step of the process is to file for your MOA (Memorandum of Association) and AOA (Article of Association), along with all the necessary documentation.

4. Apply for Your License

Once you have secured your MOA and AOA, the final step of the process is to submit all your documents to the RBI, along with your incorporation certificate and INC-12 form to obtain a license. Some of the most significant documents you will need to submit in order to secure a license for your microfinance business are as follows.

- Documents for identity proof of all directors as well as promoters.

- Documents for address proof of all directors as well as promoters.

- Photographs of all directors as well as promoters.

- Documents for proving ownership of registered office or rental document.

- NOC from the property owners

- Stamp duty as prescribed by the state

- Any other document which might be prescribed by the state government.

As is evident from the above explanation, it is much easier to register your microfinance business under Section 8 of the Companies Act, 2013, as compared to registering it as an NBFC.

In Conclusion

As the demand for microfinance institutions continues to steadily increase among the Indian populace, in my opinion, starting a microfinance institution is the need of the hour. Now that you know how to get started with the registration process, go ahead and register your very own microfinance business in India today.

All the best.

The Reference Shelf

- Microfinance Company Registration [Link]

- Growth of Micro Finance in India: A Descriptive Study [Link]

- Chapter 1: Introduction [Link]

- Microfinance industry sees 31% rise in loan portfolio at Rs 2.36 lakh crore in FY20: Report [Link]

- All About MicroFinance Company Registration– The cheapest way to start the Micro Finance Company in India [Link]

- Gross loan portfolio volume of the microfinance industry in India from FY 2012 to FY 2016 [Link]

- How to Register a Micro Finance Company in India – A MFI – NBFC in India [Link]