The pandemic has been hard for many sectors. This was true as well for the Microfinance industry. Collections had dipped by April 2020 as the first wave ripped through the country. And even prior to that, the sector had already been facing competition from banks as well as from fintech who were using technology to reach out to more underbanked and unbanked customers.

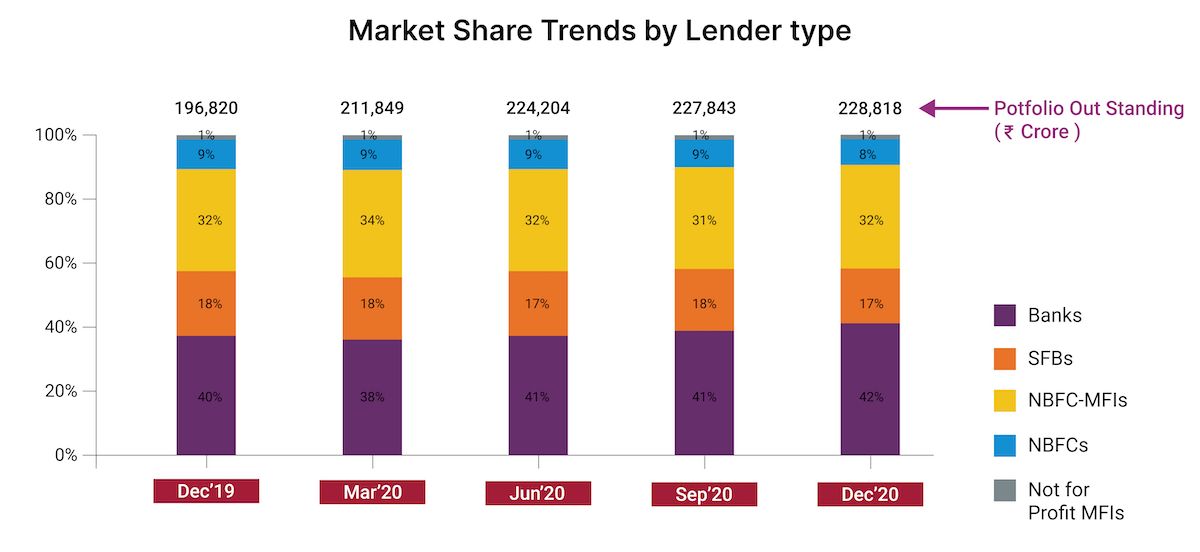

But even today, while banks have 50% share of the market, NBFC MFIs and NBFCs together account for 37% of the market according to MFI Pulse Report, SIDBI and Equifax, April 2021. This makes them critical for the financial inclusion needs of the country.

And 15 months from the beginning of COVID-19, there are signs of change. A recent ICRA Ratings report spoke about a robust long-term outlook for the sector with improvement in disbursements and collections in 2021 which can help the industry achieve 9-11% AUM (assets under management) growth in FY 2021.

Not just that, another possible shot in the arm came from a 2021 RBI proposal which, if passed, could level the competitive playing field between NBFCs and banks and remove some of the restrictions placed on the sector post-2010 to counter allegations of lending malpractices. First, the interest rates, the proposal states, could be decided at the Board level of each company, after considering all risk factors. Second, the earlier ruling that no two MFIs could lend to the same borrower could also be removed.

Both factors could spell growth and positive momentum. If risk is managed proactively. The focus now seems to be on rebuilding and on growth. A key part of that for NBFCs is to get access to more capital to plan for scale.

Traditionally, we have seen two paths to scale for NFBC – a direct listing for IPO or shapeshifting into a small finance bank and then listing. Let us evaluate each and its possibility.

The two paths to growth

Let us take you back to 2010. It was a heady time for the sector. SKS Microfinance was the first NBFC at that time shooting for an IPO. But the story also had a cautionary tale. The plan was overambitious. Soon after the IPO, suicides of rural borrowers in Andhra Pradesh brought a different colour to the story. And the string of restrictions then placed on the industry to stop the possible malpractices, also restricted growth. The companies that found growth posts that, had to look for a slightly different route.

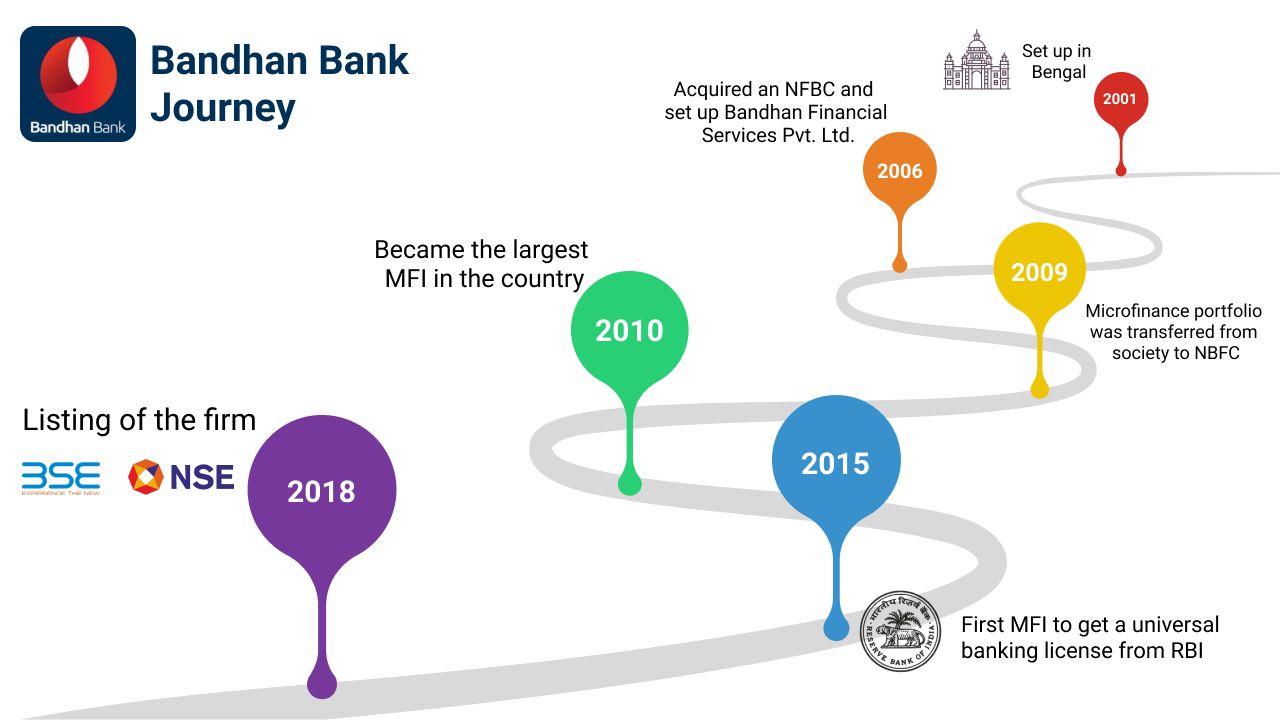

Meanwhile another story was being written in the Microfinance industry. The path to scale here was different. The firm? Bandhan Bank.

2001: Set up in Bengal

2006: Acquired an NFBC and set up Bandhan Financial Services Pvt. Ltd.

2009: Microfinance portfolio was transferred from society to NBFC

2010: Became the largest MFI in the country

2015: First MFI to get a universal banking license

2018: Listing of the firm

Listing, in this case, happened 17 years after setting up andthe rroute was through first setting up the banking operations.

There were lessons learnt also from Equitas and Ujjivan IPOs which were more socially focused. Given the regulations post-2010 restricted their ability to go beyond microloans, they became small finance banks, with approval from RBI, which helped them take deposits from clients. It also forced them to reduce foreign shareholding to less than 50%. This was difficult without a public listing for some of the companies. And hence public listing was the obvious next step for growth and scale for the firms.

For companies looking at scale and growth now, the Bandhan, Equitas and Ujjivan template could provide some useful guidance.

Active investors in the sector:

The immediate action for many companies looking for growth in the sector is where and how they can find access to capital. Following is a list of some of the investment firms that have been active in this space now. They offer a mixture of debt and equity instruments as growth capital:

- Unitus Capital

- Accion

- International Finance Corporation

- Omidyar Network India

- Michael & Susan Dell Foundation

- Aavishkaar Capital

- Aspada Investments

- SIDBI Venture Capital

- Lok Capital

- Gojo & Company Inc.

- Aavishkaar

- Dia Vikas

- Developing World Markets

- Norfund

- Northernarc

- Caspian Impact

- TPG Capital

- Warburg Pincus

- Norway-based Nordic Microfinance Initiative (NMI)

- Carpediem Capital Partners

While building their investment proposals, companies can start shortlisting a similar list of investors to reach out to.

The investment readiness checklist:

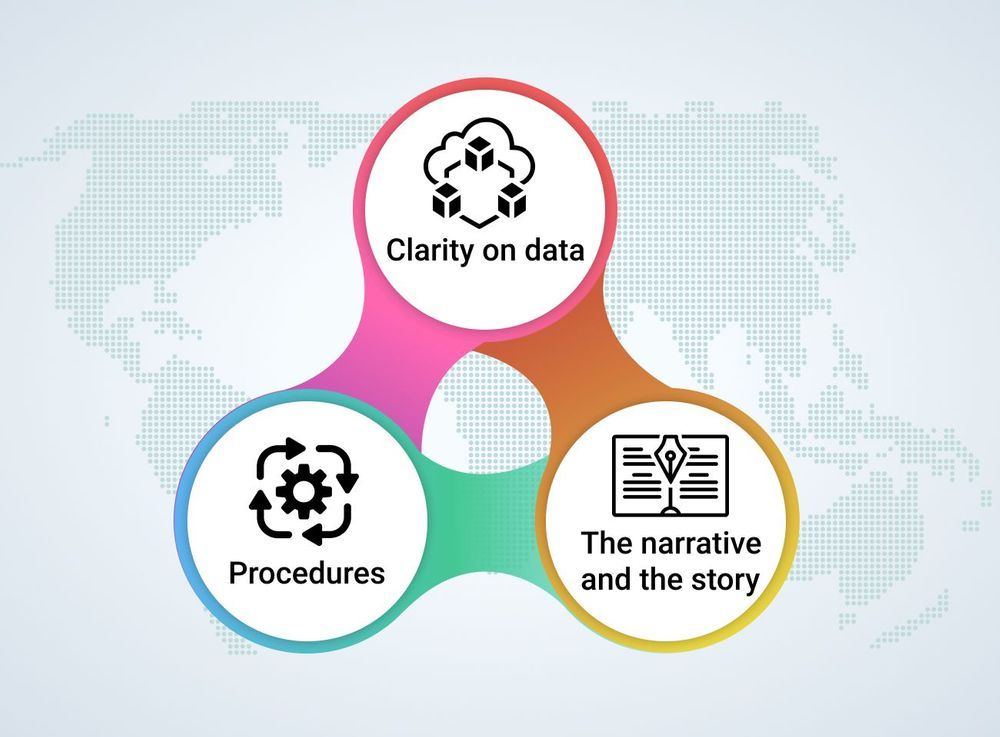

Meanwhile from the investors’ point of view, given the changes the industry has been through, they need to be convinced about the long-term growth of the company. That means extensive due diligence, a process which has only become more complicated post COVID-19. Here are a few things that investors will need and that companies need to start keeping ready as they progress in their discussions:

Clarity on data: Investors would need details on the key metrics around loan metrics, liquidity, capital. It is important to keep this information ready in a structured way for the data room discussions

Given the post-COVID world, a lot of this might have to be structured digitally and controlled access might need to be given to the investor teams.

Procedures: Just as important as the data, is the clarity around the processes that the company has set up around underwriting, risk, collections and more. Investors need to see the scale thinking behind the numbers

The narrative and the story: Investors need to understand the positioning of the company within the sector and a clear assessment of its current and future strategy which is the bedrock of the story

As we move to the second half of 2021, we are already seeing a spate of IPO announcement

Women nts across sectors. Can we see MFIs joining the listing wagon? If more meaningful investment decisions can get unlocked now, that is the growth journey we hope many MFIs will unlock. It is a journey that needs to be taken considering both the lessons learnt from the past and the way forward for the future.