")

From the co-origination guidelines released in 2018 to the ‘Co-lending Model’ (CLM) of 2020, the framework’s evolution has spurred the collaboration of banks-NBFCs. It democratized credit access for Micro, Small, and Medium Enterprises (MSMEs), Low-Income Groups (LIG), Middle-Income Groups (MIG), and Economically Weaker Sections (EWS) by bridging the gap between the geographical & capital limitations and the lending opportunities.

Let’s understand in brief the differences between the two CLM frameworks.

Co-lending has come a long way since its inception. When RBI allowed co-origination to boost the liquidity crisis in the NBFC sector in 2018, it was considered a tool to expand lending opportunities and revolutionize financial inclusion in India. Fast forward to today, co-lending is a mammoth market, estimated to reach a total volume of around INR 25,000–30,000 crores in 2022–2023, with more and more mainstream banks and NBFCs embarking on co-lending partnerships. Financial experts believe the potential for expansion from here is high.

Nevertheless, implementing the co-lending model can be daunting to both new NBFCs and established players in the market. They must manage complex operations, adapt to disruptive technologies and ever-changing market conditions, handle defaults, and collections among several other responsibilities. To stay ahead of the curve, NBFCs must address the complexities that tag along with the framework.

Before we divulge how Finflux is solving the hurdles and helping NBFCs meet their business requirements, let’s quickly recap the complexities of the co-lending model.

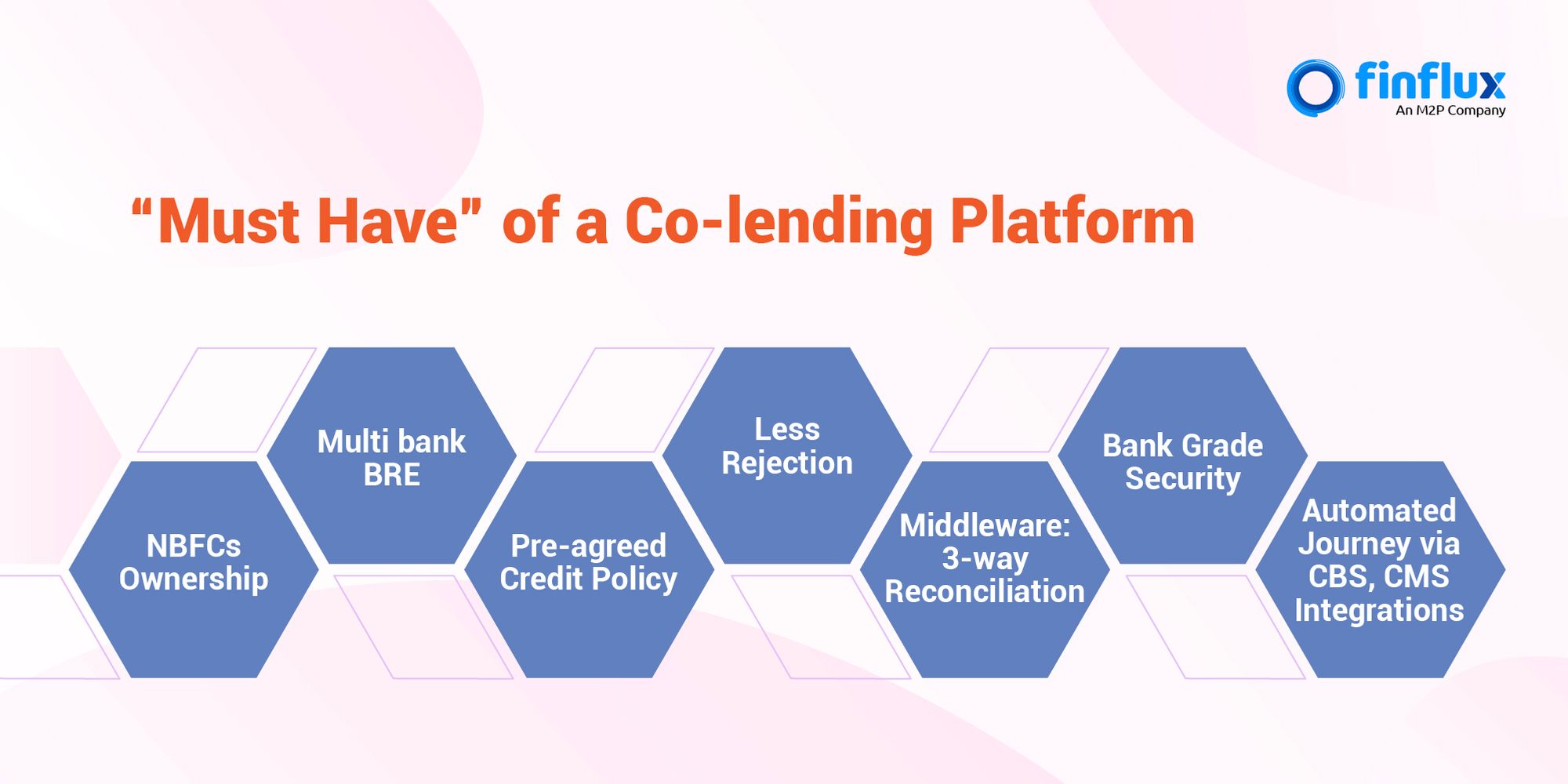

Complexities of the Model

Undoubtedly, co-lending has opened unique opportunities for formal lenders to come together and share their synergies to create a winning proposition for all stakeholders. However, they must prudently evaluate their capabilities to handle the challenges posed by the exclusive requirements of this arrangement.

Here are some of the regulatory prerequisites and business challenges faced by lenders.

- Regulatory Compliance: The co-lenders in agreement must comply with all relevant RBI regulations such as CLM1, CLM2, extant guidelines on Managing Risks and Code of Conduct in Outsourcing of Financial Services, and Master Direction on NBFC. It is important to note that the regulations for banks are different from NBFCs.

- KYC and AML Norms: Besides the guidelines, the co-originating lenders must adhere to the Know Your Customer (KYC) and Anti-Money Laundering (AML) norms without compromising the overall TAT. This calls for a smooth integration of their technology systems to exchange customer information and supporting documents seamlessly.

- Credit Assessment: The regulations mandate each co-lender to obtain a credit report from the credit bureau and perform a quality credit assessment without significantly increasing the time to approve the loans.

- Risk Assessment: Both lending partners are responsible for the risk assessment of their respective loan portions. A robust risk management strategy will ensure hassle-free loan appraisal, credit monitoring, and loan recovery processes.

- Operational Framework: The co-lender agreement involves multiple co-lending partners, voluminous loan documentation, disbursements, repayments, and more. The co-lenders should establish a mutually agreed framework for day-to-day monitoring and recovery of loans to ensure transparency and hassle-free reconciliation while handling repayments, loan charges, etc.

- Asset Classification and Reporting Requirements: The NBFCs and the banks have independent asset classification and provisioning & reporting requirements with specific accounting, reporting, and exposure calculations at their ends.

- Complex Accounting Methodology: The model requires lenders to publish their credit policies for accepting co-originated loans. It involves a complex accounting methodology that needs to be set up for the three components of co-lending: one for the borrower, one for the NBFC, and one for the co-lending partner. Further, banks and NBFCs must enter into a master agreement on loan servicing and customer service.

Finflux’s Co-lending Platform – The Ease of Configurability & Servicing

At Finflux, we recognize the requisites and practical challenges associated with the implementation and have developed a composable, API-first, cloud-native platform that allows NBFCs to onboard and manage multiple co-lending partners with ease.

The platform is a comprehensive co-lending solution that comprises the following.

✔ Onboarding & Configuration Modules: Partner onboarding with extensive co-lending & product configurations

✔ Origination: Manage complex origination journeys & workflows across partners

✔ Loan Management & Reporting: Lifecycle management with managing multiple SOAs & amort schedules

These modules enable the NBFCs to accurately track the distribution of loan funds and repayments among different lenders. It ensures all lenders receive their share of the loan repayments and that the funds are appropriately accounted for and reconciled. The platform also supports CLM1 and CLM2 guidelines and facilitates KYC/AML integration.

Here are some of the key highlights of our co-lending platform:

Partner Configuration

Each time an NBFC wants to get into a strategic partnership with a bank or a lender, they do not have to go through the tedious and time-consuming process of onboarding the partner. The platform entitles NBFCs to quickly and efficiently onboard a partner by configuring capital contribution, hurdle rate, principal & interest computation strategies, repayment strategies, types of co-lending (accrual/cash-based), and instant/deferred contribution. Additionally, they can both onboard multiple partners across their product range or configure different products under one partner.

Charges & Waiver Configuration

Finflux offers a range of charges and waiver configurations that allow NBFCs to customize their fees and waivers according to their specific needs. This allows them to assign a percentage to different charges to calculate their contribution toward a loan. The charges contribution percent feature enables them to accurately calculate charges, the 50+ charges configuration feature provides flexibility and customization, and the waiver management feature helps NBFCs build stronger customer relationships.

Repayments & Splitting

NBFCs can define the capital contribution and hurdle rate for transaction splitting while onboarding a co-lending partner. It can be reported not only in terms of funds but in other facets too: accrual, interest income, fees, penal charges, foreclosures, part-payments, waivers, etc. Further, the platform facilitates NBFCs to do collections splits in two ways: paying the co-lender first and then the originator or paying both parties simultaneously. Also, NBFCs can set up principal and interest computation strategies to define the repayment schedules.

Escrow Management

The platform’s escrow management system works in tandem with Payment Gateway partners – it simplifies and streamlines the process of creating and managing escrow accounts, disbursing loans (either instantly or in bulk), reconciling transactions, and updating ledgers automatically. Lenders can swiftly create escrow accounts and configure the disbursement process to meet their specific requirements, including setting the loan amount, the disbursement date, and the repayment schedule. The auto-update ledger feature saves lenders time and resources that would otherwise be spent on manual ledger updates. Finally, the synchronized Loan Management System (LMS) for Loan Account Numbers (LAN) updates ensure lenders have access to the latest loan information.

Loan Origination System

The platform offers a comprehensive LOS with co-lending workflows, Business Rule Engine (BRE) capabilities, risk level versioning, and lead allocation logics, and can support any distribution model. These attributes will enable lenders to achieve the following:

- Collaborate with multiple financial institutions

- Configure and customize the credit assessment and due diligence modules based on the decision parameters from the partner’s credit risk team

- Maintain different versions of credit policies and decision-making models

- Configure multiple loan views for different loan products

- Define lead allocation logics based on various factors such as geography, loan amount, or product type

Accounting & Reporting Management

The account management system empowers NBFCs to configure GLs for each product by defining fund source, interest payable, contribution name, and account. The reporting management system supports multiple stakeholders and their unique reporting needs. It provides customizable reports, audit trails, master maintenance, and regulatory reporting, all within an SOA-based architecture that ensures scalability and integration with third-party systems.

Why is Finflux the Ideal Co-lending Platform for any Enterprise?

Finflux supports all the functions of a typical co-lending process, such as loan origination, risk sharing, loan disbursement, servicing, reporting, administration, etc. Our solution reduces the dependency on manual intervention and slashes the turnaround time when onboarding new clients and tracking collection splits.

Most importantly, Finflux can be leveraged in two ways – either as a SaaS product or can employ its extensive APIs to integrate its LMS / LOS capabilities. Additionally, it supports over 50+ 3rd party APIs via HubEX or the API bus to connect to other enterprise systems assisting real-time data exchange and a seamless user experience.

In summary, Finflux has the experience and exposure in catering to NBFCs irrespective of their structure, size, industry experience, management styles, and approaches to risk management. The customizable, scalable, and technology-agnostic solutions facilitate enterprises to rapidly deploy complex co-lending processes to scale lending operations regardless of their unique needs and circumstances.

To experience the ease and agility of our platform, schedule a demo.