On 19th December 2020, the front page of the Times of India, one of the country’s leading newspapers, carried the headline, “Humiliated by loan app financiers, engineer commits suicide in Hyderabad.”

While at first glance, this incident might appear to be isolated, however, in reality, this was just the tip of the iceberg.

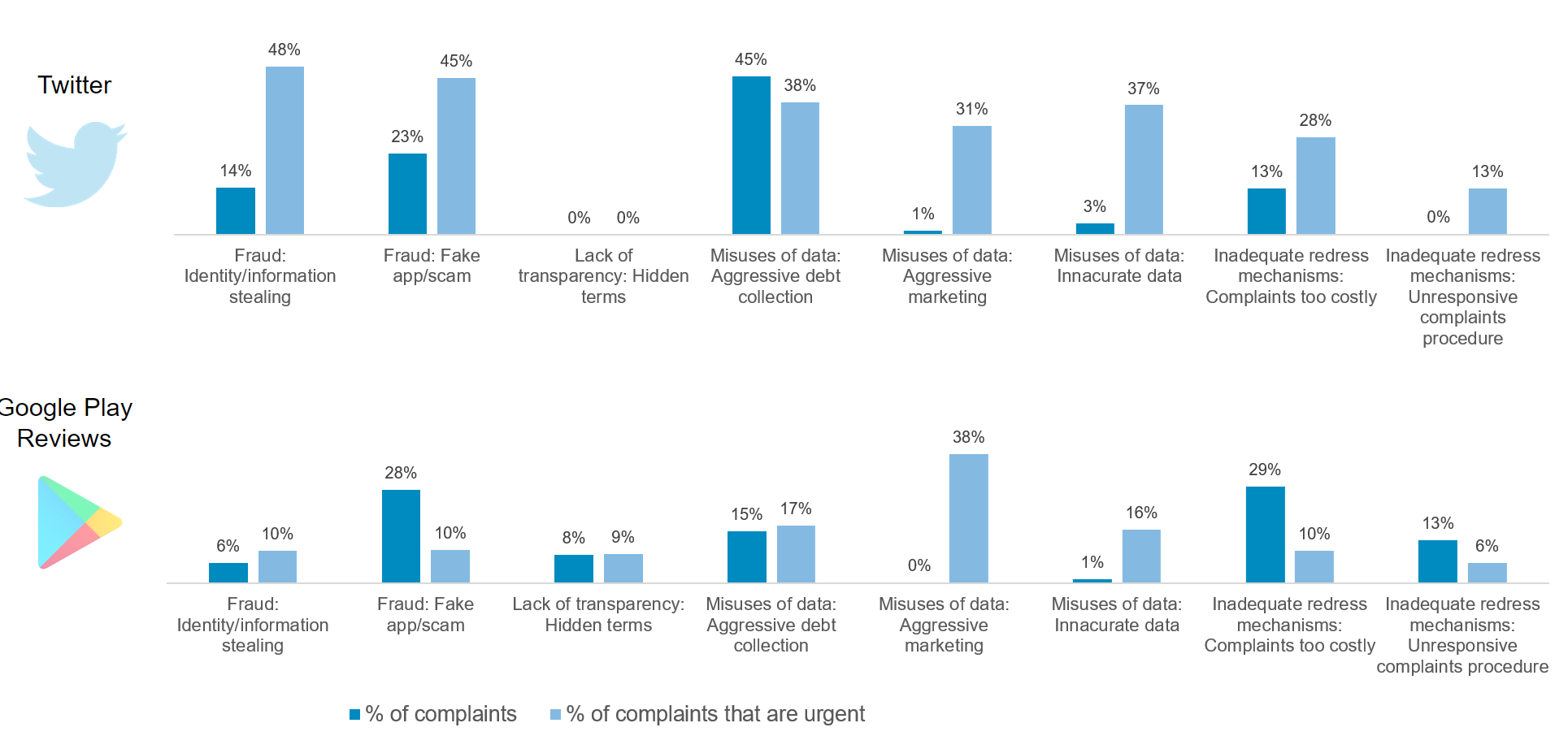

Starting at the latter half of 2020 & all the way into the mid of 2021, several consumers from every corner of the country took to social media & app store reviews to complain about the indecent & aggressive debt collection strategies lenders are following & it goes without saying that this attracted the attention of not only the press but also governing bodies such as the RBI.

Thus, in today’s blog post, we will take a closer look at exactly what is happening & try to understand the risks digital consumers might face in regards to credit access as well as its repayment.

Without further ado, let’s get started.

The Credit Access Problem in India

Credit access has been a problem in India since the very beginning & while it might seem that some segments of borrowers such as MSMEs are gaining more access to formal credit instruments, thanks to government intervention, the reality remains that these beneficiaries represent a very small portion of the populace.

According to a 2017 study by the London School of Economics, only about 10% of Indians had access to organized credit instruments & if recent surveys are accounted for, that number is not more than 20%.

As is evident from this, a large section of the country either does not have access to formal credit instruments or solely relies on unregulated markets for their needs.

However, since 2019 there has been a consistent rise in the number of digital lenders aiming to change this scenario.

Fueled by ever advancing fintech technology, India is now host to a growing number of digital lenders who solely specialize in rendering digital credit instruments to consumers, either in the form of personal loans or credit lines.

While a few of them operate via websites, the most common method via which they can be accessed is by downloading them from the Google PlayStore or Apple AppStore.

As per a survey conducted by CGAP in 2020 (Consultative Group to Assist the Poor), there are approximately 200 digital lending applications available across the Google PlayStore & Apple AppStore in India & this is after the recent removal of 30 applications on illegal lending grounds.

At its essence, these digital lending applications adopt either of three working models.

- Extension of a Financial Institution – In this case, the digital lending application is a direct extension of a financial institution such as a bank. Instead of developing a holistic banking application, several financial institutions are now adopting a strategy wherein key functions are spread across applications in order to capture a larger market share.

- Extension of an NBFC – Similar to the earlier instance, in this case, the digital lending application is a direct extension of an NBFC that is a non-banking financial institution. NBFCs usually develop these applications in-house such that greater market demand can be quickly fulfilled by focusing on one market demand at a time, rather than several at once.

- Partnering With an NBFC or Financial Institution – Last but not least is a partnership model wherein a fintech company develops a digital lending application &, at the back end, tie-ups with an NBFC or financial institution to secure capital. At its essence, this is a win-win model for both the stakeholders as the financial institution, or NBFC can leverage the prowess of the fintech company to reach & acquire more customers, while the fintech company benefits from gaining easy access to capital.

Now, while the first two business models are heavily regulated by the RBI (Reserve Bank of India), as both the financial institution as well as the NBFC needs to acquire a license to extend consumer loans to borrowers, the third business model is where the problems begin to appear.

Until the later half of 2021, the RBI had no laws in place to regulate & monitor these digital lending solutions, which further added to the problem. At its essence, since the fintech applications, which is the face of this partnership, did not need to publicly report either the NBFC they are partnering with or publicize their rules, regulations & guidelines in terms of servicing digital loans, they were essentially left to self regulate themselves which is a flawed & biased concept, to say the least.

As per the CGAP report, more than half of these supposed lending applications on the PlayStore & AppStore were fraudulent & illegal & this became widely evident both by scanning their review sections as well as tracking consumer’s digital activity on social media websites like Twitter.

The most notorious of these applications not only constantly harassed borrowers for repayment but also employed various vigorous debt collection techniques, such as sending collection agents to their residential, current & office addresses, constantly reaching out to individuals from the borrower’s contact list & even several instances were reported where these applications accessed private gallery images of the borrowers & threatened to make them viral upon late repayment.

The CGAP survey focused on studying a sample size of 150,000 publicly posted reviews of online lending applications & by leveraging NLP (natural language processing) techniques, they were able to conclude that in this subset, the consumer to complaint ratio currently stands at 0.25.

However, while this might appear to be insignificant, it needs to be taken into account that those who were affected the most primarily lacked the skill of posting their reviews online, or we lack the tools to properly analyze them.

Along the same lines, it can also be safely concluded that a few bad apples are inflicting severe harm not only on the mindset of borrowers but also on their credit access & trust in the future, all of which has a significant negative impact on the digital lending industry.

Conclusion

In November 2021, the RBI proposed setting up a working group to monitor the state of digital lending in the country, especially via mobile applications & also proposed the formulation of various rules & regulations to properly oversee their activities & counter consumer harassment & betrayal right at the forefront.

However, the real life impact of these claims by the RBI is yet to be witnessed & in the meantime, several digital lending applications continue to rampage the lives of unsuspecting borrowers across the country.

Thank you for reading & I will see you in the next one.