Indian Microfinance has definitely come a long way from the initial days and has been a force of good in the lives of millions from the underserved segments of the population. There have been certain missteps, such as the emergence of fly by night operators and over-lending in certain pockets, which were handled in self-correcting and timely manner. Also like any other industry it has seen corporate misgovernance as well as non-conducive regulation from time to time. It learnt its lessons and seems enroute charting newer and higher grounds.

However, no industry can sit on its past laurels. Competition is always around the corner. In order to stay competitive any industry needs to keep reinventing itself from time to time. In the current age where technology changing faster than an eye blink, competition may not come from another MFI rather from a completely different industry altogether. We see it happening with Microfinance where “Neo Banking Companies” and “FinTechs” have started chipping away.

In order to stay relevant in the lives of customers, MFIs need to keep re-inventing themselves. In this last part of the series, we delve into areas where MFIs need to focus for the next phase of exhilarating growth.

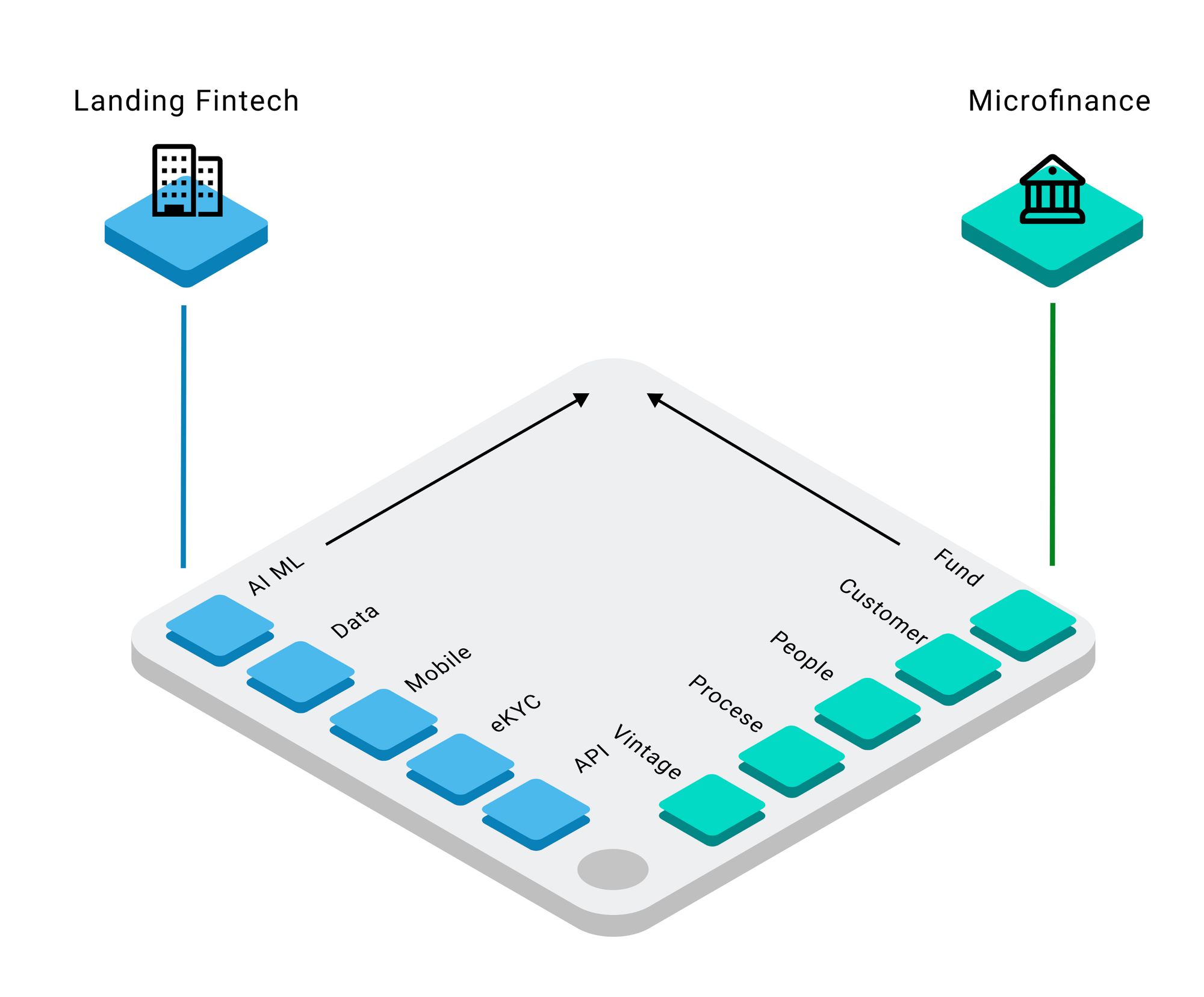

We can put competitive positions of MFIs against FinTech’s/Neo banks, which sets the context for ensuing discussion, through the following figure.

Customers’ vintage

We argue that Fintech companies do lack in terms of clients’ vintage (in their system), but they make that up with technology when it comes to customization of products. However, not having vintage, robs them chance to offer larger ticket size.

Whereas MFIs miss out on lucrative vintage borrowers’ segment, who have gone through multiple loan cycles with MFIs and despite investing heavy in clients’ onboarding and financial literacy trainings, on account of unsuitable products and processes.

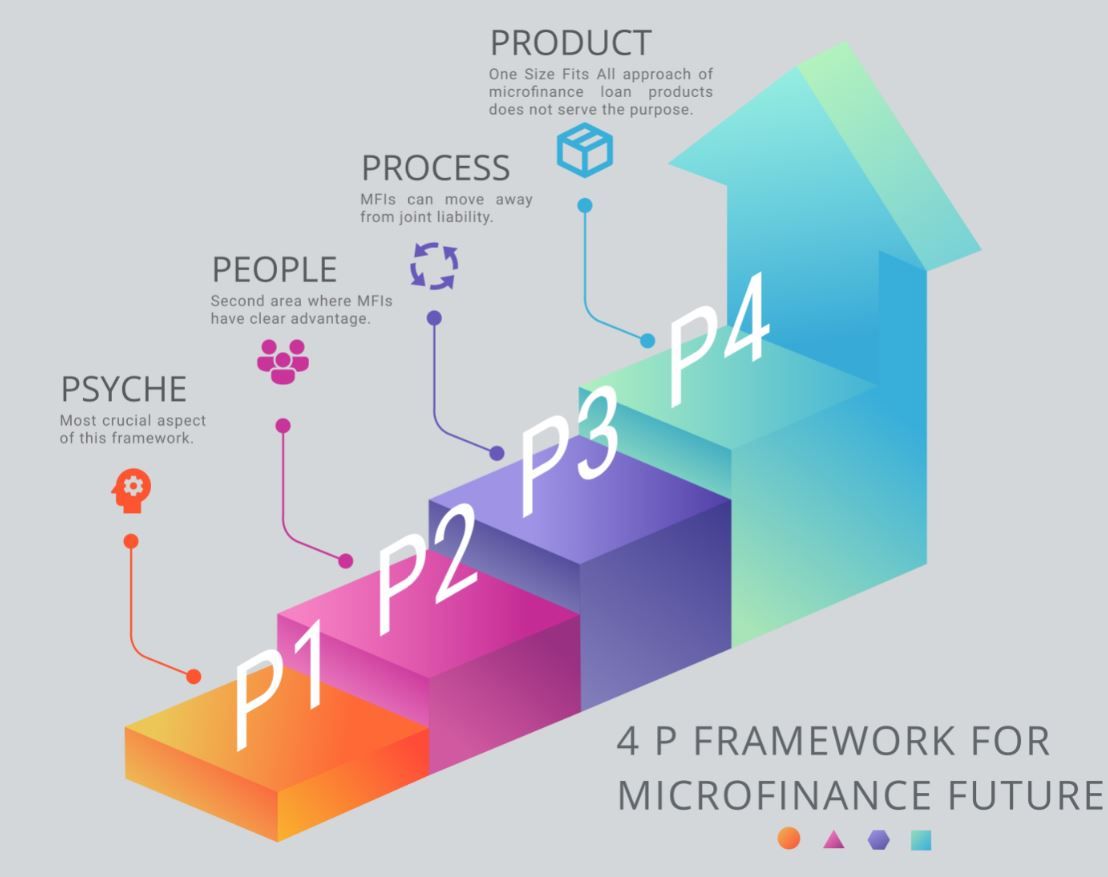

4 P framework for Microfinance future

In order to have continued customer loyalty, MFIs should move fast otherwise they may lose to the new- age competitors. Action areas where MFIs need to rethink can be summarized as 4Ps. This framework is evolutionary in nature. By that it is meant that each step will lead to the subsequent one.

Psyche

This is the first yet the most crucial aspect of this framework. It starts with MFI leaderships, for the Board of Directors and Executives, acceptance of the need to rethink their business. As a major portion of MFI loans helps the poor start new ventures. Hence like all enterprises, these enterprises need primarily long term and patient capital while setting up their businesses. On top they need other financial solutions such as short-term working capital loans and suitable insurance solutions in addition of life insurance. In short, MFIs need to start offering end-to-end enterprise business solutions. It all starts with philosophy metamorphosis.

To MFIs’ advantage this is where they have a clear edge over neo banks because of they understand small entrepreneurs better. MFIs have higher risk-taking capacities hard wired in their DNAs. This requires change in perspective for MFIs to start behaving like a financial solution providers and not just a lender anymore.

People

Second area where MFIs have clear advantage yet need to go deeper is their frontline staff’s quality and their skillset. Unfortunately, in order to grow rapidly staff onboarding/grooming process is a casualty. MFIs with better financial resources, in order to jumpstart, get staff from other established players. However, that may not always be the smartest strategy because frontline staff quickly shifting organizations may have short-term view which can be riskier while making credit decisions.

To counter this MFIs, need to start investing in their human capital and look at their staff for what they are, capital. Given the competition they are going to face from faceless entities, which can extend loans at cheaper rate as well as quicker turnaround time, one clear advantage MFIs have is the human touch they can provide to its clientele. However, the need is to make this human touch more than just a formality This physical touch point needs to provide data points, mostly qualitative, which cannot be collected using smartphone as interface. As the clients need constant upgradation, similarly loan officers also need to be upgraded in a timely manner.

In order to attract the brightest of potential employees, profile of loan officers need to look attractive with right messaging related to role’s decision making power and long-term career path. Once in the system, they need to be groomed to understand complex business issues and shouldn’t be treated dispensable resources.

There is definite need to make workforce, at least the frontline one, more inclusive. This could be done having better representation of female staff members as well as individuals from other less represented social groups such as minorities and scheduled castes. This along with being an important social initiative, is equally suave business decision. This will ensure that MFIs have closer ears to ground in terms of customer, who are mostly female, feedback as well as needs.

Process

Ever since evolution of JLG model most MFIs follow the same model of female JLGs wherein groups’ social capital is treated as collateral. In case of defaults, risk is shared by the remaining members. This becomes a major roadblock as the loan sizes increase. There is no individual credit history of clients leading to false impression of credit discipline being impeccable which often leads to defaults with bigger loan sizes. Secondly loan sanctions and amount decisions are intuitive. Mostly the only decision that MFIs take is whether to sanction or not? That too is dependent on the Credit Bureau check and thus is “Go” or “No Go” decision.

However, thanks to ubiquitous presence of mobile phones, there are many alternative data points available, which were not there when these processes were designed. MFIs need to make full use of this treasure trove of non-financial data points such as social standing of the family or who takes decisions in the family. These data points can be put into a data engine and MFIs can come up with decision of either lending or not lending along with loan limits of individual customers. With this capacity MFIs can move away from joint liability and start treating group for what it stands for today, distribution mechanism.

Product

What is true about processes being outdated, is even truer in case of products. The entire financial landscape has undergone a massive change ever since MFIs started flourishing. However, MFIs haven’t innovated enough with financial products but for small tinkering (it can be argued that it was too under crisis situation and with enough RBI prodding) with the loan tenure. It is as Almost nothing has changed in the last 25 years

Pure vanilla loan products may be good for any MFIs’ initial scale-up but those don’t do much to satiate demand of an evolved clientele. Current “One Size Fits All” approach of microfinance loan products does not serve the purpose of many segments such as agriculture and stationery shops because of high seasonality. This calls for lot more efforts to be put in to understand customer needs, especially for those who have evolved through the process. Need of the hour is to customize these products to the requirements of the customer and not the other way around. Collection of data points, building personas and evolution of products is the way forward.

We do recognize that the way out proposed above is easier said than done. It would require putting away traditional thinking ways of MFIs. They have done well so far reaching out to segments considered

unbanked so far. It builds inertia to do anything anew. But doing what was good once many not keep customers delighted always. MFIs need to keep thinking out of the box to have customers’ continued loyalty.

Having presented three distinct phases of Indian Microfinance i.e., history, present as well as future, we can safely say that the Indian Microfinance has evolved to great heights despite misgivings of its critics and in the process has gone through various tribulations by fire. Now that it has come to make a distinguished name for itself, it needs to be ready for the next phase of this growth which will put continued existence and relevance beyond doubt.

With the recent RBI consultation paper, the regulator seems willing to take the first step in the direction of harmonization of microfinance. However, MFIs also need to prepare for impending competition from bigger and better capitalized players such as Banks along with new age players. During this phase MFIs shouldn’t hold to legacy mentality (so far unbanked would value us more for we provided them services first) will be counter-productive. It is time to take this opportunity with both hands and run with it. MFIs have put in all hard yards in getting unserved sections financially mainstreamed. Now they should make full use of this opportunity and build upon. Time is now for MFIs to keep updated on technological tectonic shifts upending all industries and be aware that they can’t remain immune from it happening in microfinance. Now they are too big to fly under radar. So better to put their straps on and fly.